“An economic rule states that one should never underestimate the inability of free marketers to use common sense,”

K J Galbraith 2006. Lincoln Journal.

One of the interesting aspects of the current debate on the behaviour of China towards Australia, after Australia asked for an enquiry into the source of Covid19, is that many of those who are well known as journalists and commentators, and even some hopelessly naive Australian politicians, and we have our share of them, have shown most clearly that they know little to nothing about the art of negotiation or as many of us know it by another name ‘bloodless warfare.’

It is well known that when it comes to selling their wares farmers around the world are weak, some weaker than others. It is also well known and oft quoted the statement by President J F. Kennedy “The farmer is the only man in our economy who buys everything at retail, sells everything at wholesale, and pays the freight both ways.” These days we would say ‘person’ but the statement remains correct. The question is what have farmers done, particularly in Australia, to redress what is an iniquitous situation?

The answer of course is nothing, certainly nothing that has lasted. Co-operatives been tried, some may still exist, but the power of agricultural cooperation in Australia is as dead as the proverbial maggot.

![]() Farmers have tried cooperation; the most famous in Western Australia being Wesfarmers. A hugely powerful organisation started by farmers for farmers and it served them well for many years.

Farmers have tried cooperation; the most famous in Western Australia being Wesfarmers. A hugely powerful organisation started by farmers for farmers and it served them well for many years.

Formed in 1914 it guided and supported agriculture in Western Australia through the Great Depression and the difficult times post WW2. Then in the sixties and seventies alongside it’s major competitor Elders G M, agriculture in WA soared as we cleared a million acres a year.

Wesfarmers was listed in 1986 and there is a good argument that it was at that time, that it started to lose its farming roots. The St George’s Terrace Harvard types took over, looked at the assets and decided they were underemployed, which they were.

Wesfarmers sold off their agricultural business to of all people The Australian Wheat Board (AWB), and what a disaster that was. Talk about failing to stick to the knitting! That saw the end of the deregulated AWB as well. What a disaster.

The Wesfarmers Group is now one of the biggest and diverse conglomerates in Australia, it is heavily reliant on China and agriculture has long gone out of its portfolio. The abandoning of agriculture by Wesfarmers should have been rejected by the shareholders, but farmers lost their voice and their control in their cooperative when the city ‘suits’ took over and floated the business. The connection between the city and the country, that had sustained Western Australia through good and bad times, was broken for ever.

Farmers hastened the demise of cooperation. Realising they could do little to influence what they received for what they produced, they became hard nosed purchasers, driving down the prices they paid and at the same time, though they didn’t realise it, reducing competition in the supply marketplace which in turn drove them into the hands of a few powerful suppliers.

As those suppliers became strong so they put pressure on those who supplied them, chemical firms and the like. I have known resellers sell to farmers almost at their purchase price and live off the under-the-counter bonus they received from the manufacturer. Nobody won in the end because many small country towns lost their suppliers, their people and their soul.

The dairy industry in Australia is a perfect example of how to ruin an industry by allowing government to stick slavishly to the dictates of the free market economy. The two main supermarkets sell 60% of the dairy products sold in Australia well over 50% of fruit and veg and the latest figures put meat at somewhere close to 70%, that is market control. When our dairy farmers are on their knees why are we importing dairy products from New Zealand and the EU?

The failure of the cooperatives was that they never saw it as their mission in life to value add to what their farmer members produced. Their Boards, mainly made up of farmers, didn’t see it as their objective, goal or something positive, to say, build a meat works and control the market from the paddock to the plate both in Australia and for export. Vertical integration was not for Australian agriculture and it still isn’t.

Instead of building meat works sheep producers relied on live exports. Millions of sheep a year were put on the boats under the pretext that there was no refrigeration in the Gulf and places like that. The pretext was a lie, it was engineered by the exporters and the meat processors.

I remember selling 4 tooth merino wethers in good order for a price insufficient to pay their freight from Geraldton to the meat works or the ship, they were bought by Thomas Borthwick.

A few days later I flew to England to see my Boss and tell him of the tough year we were having in the Chapman Valley. While there, at a market in Clitheroe, I saw some woolly old black-faced mountain ewes, not a patch on the wethers I had given away in Midland, sold for £26 a head. I think the exchange rate was two dollars to the pound, so A$50 per head. The buyer in Clitheroe was, Thomas Borthwick. Mutton is mutton the world over. God knows what those merino wethers made in Dubai or wherever they went to finish in the boot of someones car.

A few days later I flew to England to see my Boss and tell him of the tough year we were having in the Chapman Valley. While there, at a market in Clitheroe, I saw some woolly old black-faced mountain ewes, not a patch on the wethers I had given away in Midland, sold for £26 a head. I think the exchange rate was two dollars to the pound, so A$50 per head. The buyer in Clitheroe was, Thomas Borthwick. Mutton is mutton the world over. God knows what those merino wethers made in Dubai or wherever they went to finish in the boot of someones car.

The farmers who ran the co-ops in Australia didn’t build woolen mills either so they could export cloth and yarn and maybe clothes to the world. Why they didn’t do it God only knows, because with a couple of hundred thousand migrants arriving from the UK, Italy and Greece every year from the end of WW2 , it could have been done.

As I wrote the other week we, the wool growers who controlled the biggest wool production pipeline in the world paid tens of millions every year to the International Wool Secretariat so they could oversee the demise of the Australian wool industry when it should have prospered.

Fast forward to today and there is many a fruit and vegetable grower who will be honest in private and seldom tell their story in public when it comes to supplying the major supermarkets, mainly Coles and Woolworths.

Coles of course is part of the Wesfarmers Group, even thought they have been demerged. The poacher has turned gamekeeper and how!

There is no doubt that some of the quality and price controls that the major supermarkets put on fresh food growers in particular, are onerous. Stories of crops being ploughed in because of minor imperfections are many, and it has gone on for years. The power of the retail food chain in controlling farm gate prices and the metropolitan markets is rigorous and often harsh. They are the price setters, the rest follow.

Beef and Barley.

I started this article by claiming that those in the media who comment on what is going on between Australia and China over barley and beef, lack knowledge and experience when it comes to trading — trading like the masters, the Chinese. I say the Chinese masters because that is what they believe they are, and they are out to prove it.

I started this article by claiming that those in the media who comment on what is going on between Australia and China over barley and beef, lack knowledge and experience when it comes to trading — trading like the masters, the Chinese. I say the Chinese masters because that is what they believe they are, and they are out to prove it.

This is not a comment on China’s aggressive behaviour towards Australia, it is an observation that we should have seen it coming.

Calling China the Middle Kingdom dates from c.1000 BC, when the Chou empire was situated on the North China Plain. The Chou people, unaware of high civilizations in the West, believed their empire occupied the middle of the earth, surrounded by barbarians.

To a large degree modern China still believes that. We are the barbarians and we are to be subjugated, and the Chinese believe they now have the power to try it on.

That concept, subjugation, is nothing new in the West, we do it all the time to each other and with equanimity.

Consider what the major supermarkets Coles, Woolworths and the others have done to producers of dairy, fresh food and to the food processing industry in Australia, that’s subjugation.

The supermarkets fix the price of milk and it doesn’t seem to matter to them if the producers go broke and many, sadly commit suicide. Whoever pays the piper calls the tune and what’s more the peasants dance, don’t they? That’s subjugation.

Over the last twenty years or so China has gradually worked its way into a position where it supplies the world with it seems almost everything it needs at prices the world has been unable to match with its own industries.

China has stolen intellectual property and brazenly made the product. They have seduced many industries in the West and persuaded them to manufacture in China. Apple, BMW, Mercedes, Land Rover and Caterpillar to name just a few. No longer is China the home of the cheap and nasty, not when prestigious mechanical and electronic engineers from all over the world employ them.

China’s strategy has been to dominate world trade in steel and manufactured goods and they have succeeded. Ask Donald Trump.

In Australia we have become reliant on China for everything from steel to machinery to clothing and pharmaceuticals and so much more. Bunnings wouldn’t exist I believe, without China.

The modern bean counter doesn’t like keeping big stock inventories, they like just-in-time supply. From factory into store then onto the shelf and sold. Quick cash, low borrowings.

A good supplier like China likes that arrangement as well, because low stocks increases the buyer’s reliance on just-in-time delivery. Delay supply and the customer will agree to anything even changes in price and service. Are they now trying that on Australia with barley and beef?

Nixon got it right first time.

I worked with the Chinese in Malaysia and I was paid a great compliment when I was told I was the first ‘trader’ they had encountered from Australia and for that matter from the UK. I asked what they meant and was told that I wasn’t a salesman and that I was a change from what they were used to from Australia. Traders they said, needed a strategy and patience to implement it. A salesmen they claimed wanted instant gratification and to hell with tomorrow, and that wasn’t the Chinese way.

Patience is power; with time and patience the mulberry leaf becomes a silk gown.

Chinese Proverb.

We will see, I believe, an example of reliance on a major customer when we look at the growth in barley sales to China over recent years.

We already know about our reliance on China to buy our iron ore and coking coal. China now supplies 50% of the world’s steel needs. They have worked their way into a position where they believe they are indispensable to the Australian iron ore and coal industries — Australia’s two biggest export industries.

Agriculture Shivers.

In the last week a shiver has gone down the spine of Australian agriculture and a question has been posed regarding its trading relationship with China as China has refused beef from three major abattoirs and threatened to put an 80% tariff on Australian barley, accusing Australia of dumping.

Australian exporters, over time, have been beguiled by the size and potential of the market in China and have ignored the inherent dangers in relying on one customer, the old adage of ‘don’t put all your eggs in one basket’ has been shown to be true, yet again.

China is Australia’s biggest customer for exported barley. It pays A$1.2 billion for 4.2 million tonnes, and accounts for around 68% of Australia’s barley exports to its top ten markets.

There is a plausible argument that the threat of placing a tariff on barley after signing a Free Trade Agreement with China is a dramatic retaliation by China following Australia’s many claims that China has been dumping steel glass, aluminum and many other goods into the Australian market. I think the reasons for the threats run deeper than that.

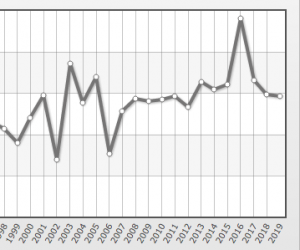

The majority of the barley that goes to China is grown in Western Australia. In 2018 about half was malting and the rest feed. In 2014 Australia exported about 1.4 million tonnes of barley to China and in 2017 about 6.0 million tonnes falling the next year to about 4.8 million tonnes. Australia’s share of the total imported barley market in China was about 70%

Barley Production Australia x 1000

13,506 MT

8,200 MT

Look at the year 2011 on Graph 2. It was in that season that Australia started, it would seem, to deliberately increase barley production, steady at first and then increasing. Then look at Graph 1, the yellow bit. Australia it seems was growing more barley just for China.

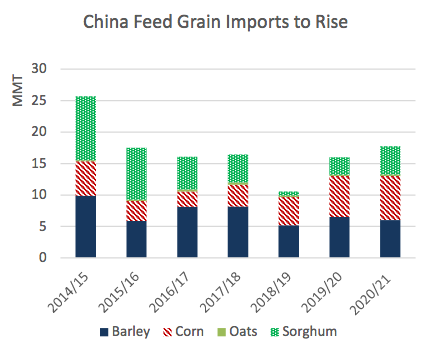

Then long before Covid19 in Wuhan disaster struck China lost 60% of its pig herd to African Swine Fever (ASF). It lost 100 million pigs to the virus and then culling accounted for the rest. China was already the world’s largest importer of pig meat, the reduction in the herd caused pork prices to increase by over 110% and the CPI by 4.5%! China started to import more beef to make up the meat shortfall.

The loss of 100 million pigs would have reduced China’s need for feed barley, peaking probably in early 2020, but imports of barley were already falling both from Australia and the rest of the world, but note the red line, stocks hadn’t fallen and malt levels remained static.

We can see from Graph 3 the extent of the damage to the Chinese economy not only from ASF but also their trade war with America. Sorghum purchases, a vital protein for their animal industries, not just pigs, collapsed in 2018/19, but corn imports, again from America, increased. Barley could have gone some way to replacing sorghum in the diet, but not all the way.

The USDA prediction shows a gradual return to a reliance on America for corn and sorghum (2019/2021) and a decreasing reliance on barley, arguably from Australia, as China replaces the 100 million pigs it has lost. It won’t take long to replace the herd, a good sow can produce 2 litters a year with 8 to 10 piglets per litter.

Whats the moral to the barley story? I think it is simple. We have responded to the ‘want to buy’ signals sent out by China in the world barley market, whether we have increased our sales to China at the expense of others I don’t know but it would seem we have because China now takes over 60% of our crop. What is evident it seems is that China has realised that it has ample stocks of feed barley for now, and that in the coming years its preference for and the availability of corn and sorghum for pig and other livestock rations, will keep its barley needs fairly stable, so this was a good time to fire a shot across Australia’s bows.

Malt for Beer.

Now we come to the serious bit. Have a look at the malting barley segment in Graph 1. It is fairly stable. Good malting barley on the international market is mainly sourced from Canada and Australia. If China reduces it’s purchases of Australian malting barley, simply by lifting the tariff, it could well deny Chinese maltsters the grain that they need to keep beer production where it must be.

Now we come to the serious bit. Have a look at the malting barley segment in Graph 1. It is fairly stable. Good malting barley on the international market is mainly sourced from Canada and Australia. If China reduces it’s purchases of Australian malting barley, simply by lifting the tariff, it could well deny Chinese maltsters the grain that they need to keep beer production where it must be.

There is another point to consider. In the 1990s The Boston Consulting Group conducted a study for the GRDC. In that study the warned Australian barley growers and breeders that the world would gradually require more sophisticated malts to keep pace with the demand for more sophisticated beers and they had better be prepared for this demand in their barley breeding programmes. (If the link doesn’t work put ‘malting barley challenge into the search)

Whether it was planned or whether it was a coincidence we may never know, but in April this year a party of Chinese beer makers visited malt producers in America and according to the report purchased malt, and apparently sophisticated malt.

It is well known that the Americans guard their intellectual property better these days than they have in the past, especially when it comes to the Chinese. Unlike us they are reluctant to sell their best grain for malting in China because there is always the distinct chance that the Chinese will find somewhere in China suited to that barley and grow it there and make their own malt.

So the Americans guard their intellectual property and sell the Chinese their best malt rather than the barley to make it.

I realise that theory in a bit Machiavellian, but isn’t that who we are dealing with? And the the Chinese come out of the whole thing without any damage to themselves and having damaged Australia —which is what they intended in the first place

Beef.

I wrote recently on the Global Farmer that Australian beef producers could well be facing serious head winds in the global beef market in the near future, especially from Brazil and India in the Indonesian market, and I also commented that Brazil was substantially increasing its penetration into the Chinese market.

I also pointed out that both America and Brazil processed their cattle at a lower cost that Australia which gave them an apparent advantage in the international beef market. China recently refused beef from three Australian abattoirs on the pretext that there were labeling irregularities, that was what they claimed but the rest of the world construed that it was all to do with Australia asking for an enquiry into the source of Covid19.

The Australian media was quick to report that Russia was sending beef to China which surprised many because Russia has a history of being unable to meet the exacting health requirements of the Chinese beef market.

To further complicate matter John Condon from Beef Central reported at the end of 2019 that the Chinese beef market was in a fair degree of chaos and made what has turned out to be a very prescient comment ‘The common view among trade sources spoken to this week has been that the latest development is clear evidence that China remains a ‘very immature, higher-risk market’ for Australian beef.’

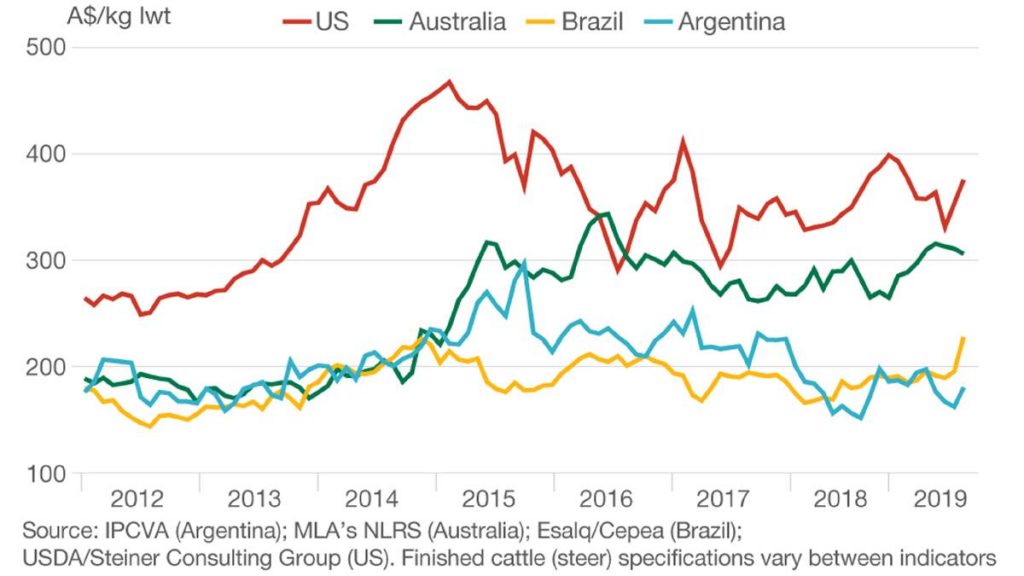

Graph 4

Graph 4

I do wonder if there is another reason for the refusal of Australian beef on the labeling pretext? Look at graph 4. At the end of last year American cattle were the most expensive of the four main beef exporters.

By 2023 the beef herd in Brazil is expected to reach 209 million head. Beef production is expected to reach 10.935 million tonnes which will represent some 20% of the world trade in beef. A new generation of professionals with multidisciplinary knowledge and a holistic vision of the productive chain proposed management practices to reduce greenhouse gas emissions in the production of grass-fed beef cattle, whose meat has high omega-3 and CLA contents – those are their objectives.

There is a large gap between the price of cattle in Brazil and Argentina and America and Australia. Argentina and Brazil have the cheapest processing costs followed by America with Australia by far the most expensive. Brazil has also been increasing its sales of beef to China of recent times, and the details are in the same article as the processing cost comparisons.

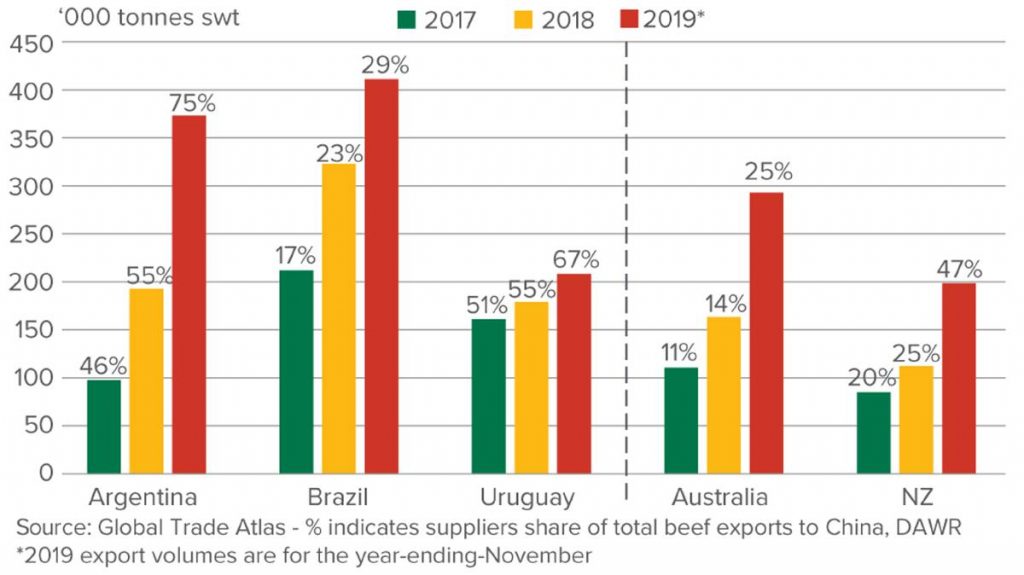

Graph 5 to me is a worry. Australia is not the major supplier to China, Brazil is number 1 and Argentina is number 2. Both of those countries had cheaper cattle at the end of 2019 than Australia, both had lower processing costs and so presumably their beef to China was cheaper than Australian beef, but maybe they cannot supply all of China’s increased needs during this time of a shortage of pork, so they are buying beef from Russia and just stirring the market pot a little? Putting the frighteners into Australian producers and exporters.

What do we do with China?

Just about everybody now realises that we have come to rely on China for too much, both for imports and for exports. We have broken the golden rule of marketing 101 which is ‘do not build a market reliance on one customer’. The barley and beef marketers have received a severe jolt from which they may not recover and from which producers will, inevitably, suffer.

And as buyers, all of us, we have been seduced by products from China which are cheaper than we have been able to either manufacture ourselves or purchase from others. We have made strategic mistakes in developing a reliance on China for vital supplies, medical equipment and pharmaceuticals to name just two. Add onto that our dependence on China for steel and metals, sixty percent of our metal nails for goodness sake! And it is easy to see how as a country we have fallen into easy ways.

We are a trading nation, but we cannot allow a policy in this country to continue where the market economy rules over national security, from defence, to fuels to beef and barley and everything in between. It’s time to stand up again for Australia and ‘Made in Australia’.

Another interesting read especially the stuff on beef competitiveness – not sure the coops ever stood much of a chance in the deregulating era of the ’80s and ’90s. Also, Woolworths runs at low profit margins (and probably at a loss in food products https://www.reuters.com/article/woolworths-grp-results/update-2-australias-woolworths-grows-half-year-profit-but-margin-pressure-hits-shares-idUSL4N1QC546 ). I reckon it’s more about lack of protectionism for Aust. farmers than market power of Woolies, Coles. Wonder if you saw this from the AFI this week? https://www.graingrowers.com.au/australian-farm-institute-briefing-paper-australian-farm-supports/ report can be downloaded at the base of the page

There are some paddock to plate coops a good one I understand is http://ncmc-co.com.au/ based in Casino. I’m not sure about your deregulation point. Farmers have little power in selling as I said, and their power in buying tends to be individual and I do believe this, together with aggregation both in farms and the service industries has led to acute rural depopulation.

I did see the Farm Institute piece, nothing new there Daniel, I have written about subsidies for years. I find it difficult having been at the sharp end of production to understand how we can compete in many agricultural markets with what is now a high cost structure and without subsidies, every advanced agric country pays more that our meager amount. The numbers you quoted for Woolies were for 2018 a better picture is here: https://www.woolworthsgroup.com.au/content/Document/Woolworths%20Group%202019%20Full-Year%20-%20Five%20Year%20Summary%20PDF.pdf

Yeah – sorry, was a bit off there with the supermarkets – thanks for the correction. Will have a browse through your archives regarding subsidies. Thought deregulation (and opening of economy) allowed new competition for existing coops and might have made other parts of the value chain (processing) less profitable than before. Will probably need to do some more reading on this and will have a browse through your site. Thanks again for the pointing me in the right direction