Australians are seriously dependent on other countries for the food they eat every day. Most of that food arrives by sea. Any interruption to supplies would materially affect the diet of the nation to the point of hunger.

It is an absolute fallacy and a hugely deceptive piece of propaganda propagated by farmer organisations and politicians to claim that Australia is self sufficient in food. Nothing could be further from the truth. In 2020 food to the value of $22 billion was imported into Australia, an increase of nearly 10% on the previous year. The retail value of that food is about $44 billion.

The food processing industry in Australia is a mere shell of what it used to be. Over the last twenty years food processors in their droves have closed their doors or left the country because they could not compete on price with food imported into this country, but grown and processed in America, New Zealand and the EU including the UK, countries who all have a standard of living equal to or better than Australia.

These three advanced economies sell to Australia, at a profit, food worth over $10 billion a year (over 50% of all food imports) and increasing annually. This food is now part of the staple diet of Australians. It is worth repeating, if for any reason the supply of this food is interrupted, the diet of all Australians would be severely stressed.

Is this the end of Globalisation and Interdependence? What it Means for Australia’s Future.

The world has been thrown into turmoil by the brutal Russian invasion of Ukraine. Every day as the Russians retreat, the bodies of men women and children, summarily executed, are found in mass graves or buried in back yards. Men with their hands bound, women raped; by the day it looks less like war and more like genocide. Europe is in shock because it cannot survive without Russian gas (LNG), coal and oil. Europe is Russia’s biggest customer for fossil fuels.

In an attempt to frustrate Russia’s invasion the world has placed sanctions on Russian exports of everything except fossil fuels. The world has frozen the accounts of Russian banks and all currency transactions. All Russian imports and exports have been stopped. The international community has frozen or repossessed the property of all the Russian billionaire oligarchs and their families, together with the assets of Russian politician’s and their families.

Russia is threatening to cut off gas (LNG) supplies to Europe unless they are paid in Russian roubles instead of Euros and Europe has said no, the contracts are in Euros. Europe knows the gas won’t be turned off because Russia needs the money.

Since the invasion began EU countries have paid the Russians €35 billion for gas compared to €1 billion it has given to Ukraine to defend itself. There is ample evidence that many countries in the EU are finding their own way, not Brussels way in this crisis and there are concerns that this show of independence may reduce the long-term value of the EU as a political force.

So much for interdependence and globalisation, particularly in Europe. It should keep national leaders awake at night struggling with the distressing realisation that they are funding the Russian invasion of Ukraine and so funding the killing of men, women and children, and at the same time they are sending rockets, missiles, ammunition and other articles of war to Ukraine, so they can kill Russians. How mad can the world get when you cannot manage your life without imports from your enemies?

Henry David Thoreau, circa 1850. ‘I trust that I shall never thus sell my birthright for a mess of pottage.’

For the sake of future generations, Australia must not give away its birthright for a mess of pottage.

I wrote the following after a long on-line discussion. It was the culmination of a larger debate about the real cost of renewable energy. I have tidied up a few phrases for clarity.

Thank you for your considered replies. I am in my eighties. My profession is agriculture from farming to science to agribusiness.

I have watched this country change substantially over the last 50 years or so. That we have largely lost our ability to be self-sufficient in some of the vital parts of our economy concerns me greatly.

Manufacturing jobs have been exported, it started way back when, when it was to Japan because their labour was cheaper than ours. Then there were others others like Taiwan, Singapore, Korea and Russia for wool. Now we have China.

There was a time we were self sufficient in food, now we rely heavily on imports, our food processing and manufacturing industry has fled due, in the main, to high power costs, much of it has gone to NZ, where they now process Chinese produce and then send it here — we eat frozen Chinese fruit and vegetables.

The news that China accounts for thirty percent of Australia agricultural exports demonstrates how reliant the Australian rural economy has become on the People’s Republic of China.

That news caused some to question the wisdom of the marketers of Australian food and wine in placing such a heavy reliance on just one customer.

That is valid question, but did you know that China buys 30% of everything Australia exports.

Agricultural exports are just a mirror image of what is going on in the rest of the country. In 2017-18 Australia exported goods and services worth a staggering $123 billion to China equal to 6.7% of the Australia Gross Domestic Product.

Mr Albanese, the Leader of the Australian Labor Party, has a poor grasp of Australian political history.

Mr Albanese recently roundly criticised Treasurer Josh Frydenberg for channeling Margaret Thatcher and the policies employed by her to ensure the much needed economic recovery in the UK following Prime Minister James Callaghan and his self inflicted demise in his ‘winter of discontent’ of 1978/79.

Callaghan finally decided to call a General Election in 1979 after the country had been ravaged for years by high inflation and unemployment. In 1978/79 strikes in both the private and public sectors almost crippled the country.

Uncollected rubbish was left to rot in the streets of London, the dead were not being buried, there was a mounting national shortage of food and fuel due to the truck driver’s refusing to work, which all combined to cause a crisis so bad the government considered declaring a state of emergency and mobilising the troops to take over vital services.

Eventually, after strikes which were violent at times, the unions got the wage increases they wanted but it was a pyrrhic victory for them. The country, the people had had enough of the militant unions shambolically and carelessly wrecking the economy, so when they got the chance they elected Margaret Thatcher to be the first woman to be Prime Minister of the United Kingdom.

In eleven years Margaret Thatcher rebuilt the UK economy and made it world competitive and respected if not liked around the world.

Albanese rejected what he saw as Frydenberg’s move to Thatcherism in favour his more Keynesian way of more and more government spending to build infrastructure and particularly social housing, for which, admittedly, there is a great need all over Australia.

Does Mr Albanese not know or does it suit his argument not to recognise that Bob Hawke and Paul Keating were the first Australian leaders to employ economic rationalism — they were the first true disciples of Margaret Thatcher?

They were Thatcherites through and through, they introduced Free Trade Agreements, globalisation and the ‘market economy’ to Australia.

It was under their government that we started to see the demise of the Australian manufacturing and food processing industry — all in the name of being ‘world competitive’.

It was also the start of a deliberate campaign to reduce the political power of agriculture in Australia.

“An economic rule states that one should never underestimate the inability of free marketers to use common sense,”

K J Galbraith 2006. Lincoln Journal.

One of the interesting aspects of the current debate on the behaviour of China towards Australia, after Australia asked for an enquiry into the source of Covid19, is that many of those who are well known as journalists and commentators, and even some hopelessly naive Australian politicians, and we have our share of them, have shown most clearly that they know little to nothing about the art of negotiation or as many of us know it by another name ‘bloodless warfare.’

It is well known that when it comes to selling their wares farmers around the world are weak, some weaker than others. It is also well known and oft quoted the statement by President J F. Kennedy “The farmer is the only man in our economy who buys everything at retail, sells everything at wholesale, and pays the freight both ways.” These days we would say ‘person’ but the statement remains correct. The question is what have farmers done, particularly in Australia, to redress what is an iniquitous situation?

“Those that fail to learn from history are doomed to repeat it.” Winston Churchill.

By the end of World War II Britain had amassed an immense debt of £21 billion (£912 billion at 2020 value). Much of this was held in foreign hands, with around £3.4 billion being owed overseas (mainly to creditors in the United States), a sum, which represented around 30 per cent of annual GDP.

Britain settled the last of its World War II debts to the US and Canada in 2006, 75 years after they were incurred.

Due to the pandemic fiscal stimulus Australia’s net debt will increase by a third this year, swelling to roughly $507 billion by the end of June 2020, which is 26 per cent of annual GDP.

John Maynard Keynes 1945. John Maynard Keynes, 1st Baron Keynes, 1883 1946), British economist whose ideas have fundamentally affected the theory and practice of modern macroeconomics.

“If farming were to be organised like the stock market, a farmer would sell his farm in the morning when it was raining, only to buy it back in the afternoon when the sun came out.” John Maynard Keynes.

Britain was unprepared for War in 1939.

In 1939 the British were totally unprepared for war, just as we are to fight a war against the corona-virus (COVID 19) pandemic of 2020. We are also an island nation like Britain.

It is a revelation to many that we import, mainly from China and America, ninety per cent of the medicines we use. We are dependent on others for our health or, to put it another way, others could make us sick by denying us the medicines we need to stay alive.

In April last year I wrote on this site that we had less than thirty days fuel, petrol, diesel, AV Gas etc in this country, and that includes the ADF reserves. We depend on the Gulf of Hormuz remaining open and we depend on China allowing our tankers in and out of the South China Sea for the majority of our fuels. Nothing has changed, we still have less than a months supply of fuel in this country.

Life would be difficult without adequate medicines and even more difficult if not impossible with little or no fuel.

It would become damned hard without imported food. It is a nonsense to claim that we are self sufficient in food, because we are not, far from it.

The National Farmers’ Federation of Australia, the National Party and the Liberal Party, together with the Australian Labor Party, all believe that Australian agriculture can raise its production to $100 billion at the farm gate by 2030.

That is an increase of 66.6% on the production of 2018 or an annual increase of about 4%, and presumably, though they haven’t said as much, they all expect the producers to make a profit every year— which is more than they do now — but they don’t tell you that.

There are some truly grim truths about the financial ill-health of Australian agriculture and they are all produced by government statisticians and the Reserve Bank of Australia.

Why these grim truths were ignored by the NFF when they set their $100 billion target, and why that target was endorsed by those who determine the the agricultural policy of this country, is for them to answer.

It would appear that there isn’t a minister for agriculture in Australia today, at both the federal and state level, who had any qualifications or hands on experience in agriculture or (agricultural) economics prior to being appointed to their agricultural portfolio. Even worse they all seem to have many other portfolios and being only human, the time they can spend on agriculture has got to be limited.

This must mean that our ministers of agriculture rely on advice from the federal and state government agricultural bureaucracies, the state and national farmer organisations and those stalwarts of Australian agriculture, the MLA and the GRDC, who are kept fat by the millions of dollars of compulsory deductions levied on producers.

Ben Rees; B. Econ.; M.Litt. (econ.)

Ben is a seriously underutilized elder statesman in Australian agriculture, probably because he deals in facts, not emotional subjective dreaming in which many in the so-called high echelons of agriculture in this country indulge.

Ben recently presented a paper to the Royal Society in Queensland. For the complete article Rural Debt and Viability click on the link above and then at the bottom of the page when it comes up click on: Ben Rees on rural debt and viability. I will try and post the complete article on this website as soon as I can.

You may not agree with Ben’s opinion — but it will make you think and make you wonder what the so-called leaders of agriculture do in their working time — time, which we all pay for.

Just a glance at Graph 11, lifted from one of Ben’s papers, demonstrates that the problems facing Australian agriculture today have not been caused by drought and will not be fixed by building new dams — the rot started years ago — it’s called debt.

Compiled From: ABARES commodity statistics Australian farm returns, costs and prices, 2006& 2018. Rural Debt from RBA, Table D9 Rural Debt, RBA Statistical Tables, online. (Ben Rees)

This is what Ben writes about Rural debt, gross value of farm production and net value of farm production: Graph 11 illustrates the impotence of the RBA to deliver required real sector policy. By 1983, GVFP was rising at the expense of NVFP. Beyond 1983, any relationship between debt and GVFP NVFP evaporates. Upward inflections in the debt curve are identifiable in 1988 and 1993 following tariff reform. Any relationship between GVFP and debt cease to exist beyond 1993; and; finally in 2003-04 the debt curve rises steeply cutting through the GVFP curve. Finally the GFC effect slows down the rural appetite for debt. From 2017, the debt curve gradient begins rising more steeply than the GVFP curve indicating that rural production is again being funded by rising indebtedness. Some good old fashioned fiscal policy was badly missing. (Ben Rees)

Nobody involved in agriculture providing they can understand basic economics like 2 + 2 = 4 – 4 = 0 can fail to see the the agricultural tragedy contained in Graph 11.

Australian agriculture has been on a productivity binge for the last fifty years. Since 1990, the gross value of farm production has grown from about $20 billion to where it is today at about $60 billion, a growth of some $40 billion or 200% in thirty years. Whereas the net value of farm production has grown from about $5 billion to about $20 billion an increase of some 300% during the same period, which looks great until we examine the debt, (red line) which has grown from $10 billion to just under $70 billion during the same period, an increase of an astounding 600%.

This increase in farm production has occurred as the number of farms has decreased. In 1970 we can see from Graph 11 that rural debt was just a few billion dollars and there were about 180,000 farms, the numbers are too small to calculate. By 2016 farm numbers have reduced to 100,000 (the NFF claims there are just 85,000 farms) and the debt has risen to ~$77 billion and by 2019 that debt has risen to $80 billion.

If we divide 100,000 by $80 billion it gives us an average farm debt of $800,000, and that is for all farms producing over $25,000. It doesn’t end there. In a publication produced by the federal Department of Agriculture and Water Resources for the Royal Commission into Misconduct in the Banking and Financial Services Industry in 2018, it is claimed that 70% of the aggregate broad acre debt was held by just 12% of farms.

On average these were large farm who produced some 50% of the total value of broad acre farm production in 2016-17. It should be noted that debt figure does not include the total credit facility limit which was estimated in the same paper at a whopping $86 billion. For many with large cropping enterprises an annual overdraft facility can, in the short term, double their debt exposure. No wonder so many feel as though they are standing on the edge of an abyss when the weather does not perform as planned.

The increasing debt levels have followed the increase in land values as shown in Figure 1. The ability to borrow against an asset, as we all know, has nothing to do with the ability to repay a debt. If the Royal Commission into Misconduct in the Banking and Financial Industry revealed anything it was that the banks were more than willing to lend against rising equity levels without determining whether the debt could ‘reasonably’ repaid by the borrower. It also showed that they showed no mercy to those who, for whatever reason, defaulted. Rural debt continues to rise at over a billion dollars a year.

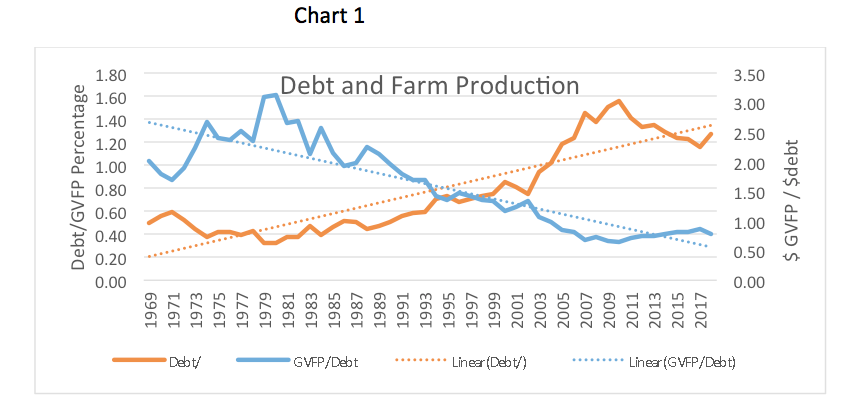

However, the alarming result of the spiraling debt, highlighted by Ben Rees, is that $1 of debt is now needed to produce 64 cents of production as shown in Chart 1. Whereas in 2003/4 one dollar of debt produced $1 of production and in 1989 one dollar of debt produced $2.14 of production. What kind of crazy economics is that?

The billion dollar question must be, ‘How many dollars of debt will be needed to generate one dollar of production on the road to achieving $100 billion at the farm gate?’ Maybe the NFF have the answer?

Have another look at Graph 11 at the widening gap between net value of production and gross value of production. That graph begs the question whether there will be an acceptable margin between costs and returns to repay what now seems to be an inevitable mushrooming of debt.

Figure 1Thatcherism

Not many in the Australian Labor Party today will recognise that those two great reformers, Hawke and Keating, were devout disciples of Margaret Thatcher, and as a result of their adoption of ‘Thatcherism’ and its mantra of ‘the market economy’ Australian agriculture suffered as market support was gradually reduced to where it is today — virtually non existent.

What Hawke and Keating and all successive Australian Governments have failed to recognise is that the adoption of the market economy philosophy around much of the free world in the eighties and nineties did not affect the huge ‘market support’ or subsidies paid to agriculture.

Without US$580 billion in annual subsidies farmers in the EU , the United States of America and almost every country around the world could not survive.

Australian producers receive world prices for their exports and have some of the highest costs and the lowest yields in the world, particularly in wheat production — their competitors also receive world prices for what they produce, but they also receive government subsidies.

Where price is king in the food markets of the world it isn’t rocket science to conclude that Australian producers face severe competition in both our domestic and overseas markets.

Have a look around the supermarket shelves in Australia and see what is imported, and what, once-upon-a-time, was grown and processed in Australia.

Australian supermarkets scour the world for the cheapest food they can buy and every time they bring more food into Australia, they put another nail in the coffin of Australian agriculture.

One of the reason that rural debt is increasing is because of land purchase. Farmers have been buying more land in an effort to benefit from an economy of scale. Fewer workers because the sheep have gone has meant bigger machinery, bigger machinery means bigger borrowing. Again, it ain’t rocket science. The quwstion is, has it worked?

The Cost of Debt Funded Production.

Let us now look through Ben Rees’ prism at farm debt over time and what producers have been able to produce with that debt, Ben writes:

Chart 1 below empirically analyses debt to output as a policy efficiency performance indicator. The orange curve is Debt/ Gross Value Farm Production (GVFP) whilst the blue curve is calculated by dividing GVFP/ Debt.

Steeply positive gradient long term orange trend curve ( Debt/GVFP)

Orange curve suggest that production has been debt dependent

Steeply negative gradient blue long term trend curve ( GVFP/Debt)

From 1984, declining efficiency as debt relentlessly consumes production

In 1989, $1 debt produced $ 2.14 in output.

By 2003-04, $1 of debt produced $1 of output

In 2010, $1 of debt produced 64 cents in production

From 1993 to 2013, sectoral performance lies below the negative sloping blue trend curve.

By any reasonable assessment, Rural Adjustment has not delivered theoretically expected outcomes from economies of scale, increased efficiency and rising productivity. Post 2003-04, both curves identify debt funded output as inefficient and unstable. Any other sector would have demanded a change in policy direction; but, agricultural leaders appear to have strongly believed the rhetoric of market theology that reduced farmer numbers structuring economies of scale would ensure long term sectoral viability. That simplistic arithmetic approach by industry leaders, major political parties; and, commentators has been a gross violation of established economic knowledge.

Ben is right. We must conclude that there is no plan for agriculture in Australia apart from that being offered by the NFF and endorsed by all political parties. What does that say for their understanding of established economic knowledge?

Is debt going to strangle Australian agriculture?

In October 2018 the National Farmers’ Federation (NFF) presented Australian agriculture with an enormous challenge —a vision for the future:

17th October 2018

The National Farmers’ Federation (NFF) has laid down a bold vision for the industry: to exceed $100 billion in farm gate output by 2030.

Based on our current trajectory, we know industry is forecast to reach $84 billion by 2030. This suggests that we still have significant work to do over the next 12 years if we are to achieve our vision.

To support their plan, the NFF have developed a road map which tells us how Australian primary producers from wheat, sheep and beef producers to bee-keepers and everyone in between what the ‘road’ is to the national farm gate producing $100 billion by 2030.

The NFF road map is complicated. I wonder how many farmers, agricultural producers and their advisers and critically, their bankers, those who lend them money, have read it — and more importantly, been able to understand both the map and their position on it?

There is no doubt that agriculture in Australia requires re-structuring. Whether the NFF Road Map is the way forward I leave for you to decide.

Is $100 billion by 2030 now the clarion cry of Australian agriculture?

To produce $100 billion of farm gate output by 2030 will require a 66.6% increase measured in dollars of production across the face of Australian agriculture in a little over ten years. Seriously? Given our recent history of growth is that figure realistic? 66.6% growth would require an annual 4% nominal growth rate in the Gross Value of Farm Production (GVFP).

There are three ways of achieving the NFF vision:

Assume that the gross value of farm production (GVFP) will increase by 66.6% and assume that yields will not and producers will make a profit or:

Assume that yields by will increase by 66.6% and prices will do what they seem to have by-and-large done over the last ten years and remain constant or decline and producers will make a profit.

A mixture of both of the above and assume that rural debt will continue to increase and producers will still make a profit.

A 66.6% increase in the dollars generated at farm gate in what is now just 10 years is a massive ask. Maybe the NFF are banking on new rural industries to help reach the target and well they may, but realistically, surely, the heavy lifting will have to be done, as usual, by the producers of wheat and beef and to a lesser extent canola, wool and sheep meat.

If there is one common thread that runs through all of the research I have put into this article so far, it is that Australian agriculture faces global challenges from ernest competitors who can produce and ship product into markets where we are active at a price which Australian producers would find and more importantly are already finding, difficult to match.

Australia has a large range of different beef products to offer overseas consumers but needed to differentiate itself from competitors through better communications and messaging, the MLA said. Photo MLA.

Our reputation for quality is appreciated by those who can afford it, but as markets expand, like the exponential growth of the middle class in Indonesia and China, so too does the market for products of a lesser quality than that which is available from Australia. Prime examples are buffalo meat into Indonesia at the expense of Australian beef and Australia’s massive loss of market share to Argentina and the Baltic States in the wheat market of the same country. The last one is hard to explain when we can almost see Indonesia from two of our major export ports in Western Australia.

What do the Banks think?

The Commonwealth Bank are not as optimistic regarding growth as the NFF, their view, as a major lender, is that production will fall across all agriculture mainly due to a drop in rainfall. A 50% drop in grain production and a 40% drop in livestock by 2060 is predicted. If Australian agriculture is to reach the NFF target of $100 billion by 2030 it will need the support of the CBA.

In contrast to the Commonwealth Bank there is a publication called Australian National Outlook – 2019. The joint Chairmen of Outlook 2019 are Dr Ken Henry AM when he was Chairman of the NAB and David Thodey AO, Chairman CSIRO. The publication is a joint effort by over 50 contributors from some 24 organisations who forecast a better picture than the Commonwealth Bank, but with many challenges for agriculture and for the nation, it is worth a read.

Beware, it is complicated, ambitious and apart from some wild assumptions on climate change, (my personal bias) a very well thought out document, and in many ways it is a pity it is not a fundamental part of the national conversation on the future of agriculture.

It makes one wonder whether those in the NFF who claim to lead this fine industry really understand, seek or accept the considered opinion of others who are already major participants in the industry of agriculture in this country. What is of note is that the Australian National Outlook forecasts a far more modest growth to $80 billion in agricultural production but by 2060, rather than the NFF target of $100 billion by 2030.

The NFF say they consulted widely before settling on the $100 billion target: The NFF led a 6-month consultation effort to inform the Roadmap. It began with a Discussion Paper which distilled insights from leading experts, before commencing a nationwide roadshow, where we spoke to over 380 farmers and other industry experts to field their views. As we consolidated this feedback, we engaged regularly with industry stakeholders and experts to ensure the ideas we’re putting forward are credible and impactful.

The NFF say they have consulted with 380 farmers. They claim there are 85,681 farmers in Australia. So they consulted 0.4435055% of farmers in Australia in the preparation of their Road Map! Hardly statistically significant.

It is also reasonable to ask whether the NFF consulted with the CSIRO, the NAB and any the fifty other industry brains who contributed to the Australian National Outlook 2019 who have a different view of the future to that of the NFF.

The has been a massive loss of knowledge and skills in agriculture.

What really shook me from Ben’s analysis of the agricultural economy, is the loss over the last thirty years of experience and skill in agriculture — this must surely present this industry with a huge challenge? Again, this is from Ben’s paper:

4.1 Performance Indicator Employment

ABARES commodity statistics for 2018[i] , shows agricultural employment peaking historically in 1990-91 at 387, 000; but, falling to 279 000 in 2017-18 (29%). Meanwhile for Australia, over the same period, employment rose from 7.8 million to 12.5million (60.3%). It stretches the mind to think the decline in agricultural employment alongside such strong national employment growth is explainable by consolidation of farm size and applied technology. Agricultural policy needs to accept responsibility for this employment outcome.

The reality is that structural industry reform began with the 1988 tariff reductions which were ratcheted up again in 1991. Orderly marketing of both major industries wool and wheat were discontinued over 1989-90. It cannot be explained as mere coincidence that agricultural employment began to decline from its peak in 1990-91 as a result of technological adoption by the farm sector at the same time structural reform of agriculture began in earnest.

Chart 3 identifies empirically that agricultural employment contracted strongly across broad-acre agriculture; and, the self – employed small scale farmer. Broad-acre employment decline appears from 2002 coinciding with the worsening of the Millennium Drought. The real loss of employment though lies in the self -employed and owner manager classification from 1992 onwards. The impact of the self- employed owner manager is particularly important as that group comprised largely the part time skilled labour force residing in rural Australia. Policy driven policy of Rural Adjustment “shipping out” small inefficient farmers would seem a more logical contributor than technology.

[i] ABARES commodity statistics, 2018, Table 1.2 , Australian employment by sector.

Long term decline in broad acre employment 52% between 1992 -2018

Self-employed fall 71.4% between 1992 to 2018 (192 000 to 55 000)

Millennium Drought emerging1997-2009

GFC 2009- 2013

2013+ Current Drought

The decline in agricultural employment whilst employment in the wider economy continued to rise strongly is a damming policy indicator. If agriculture was likened to a private firm, a clean out of the board, senior management, and advisors would be expected.

How true!

In the next issue of Global Farmer we will examine whether our main agricultural industries of beef, sheep and grain, are capable of playing their part on the road to achieving $100 billion by 2030. The question must be asked can they do it and more importantly, who has already claimed they can, because somebody has? Haven’t they?

Iran’s top general Mohammad Bagheri has warned Tehran could close down the strategic Strait of Hormuz if it faces increased “hostility” SANA/AFP/File 28.04.19

In last month’s Global Farmer, I discussed the possibility that a minor conflict, or even just a few angry words on the South China Sea or in the Straits of Hormuz could cause Australia to at best ration petrol, diesel, AV gas and other fuels — or at worst, cause this country to grind to a halt within weeks. Why? Because our current fuel reserves, in January of this year stood at 22 days’ worth of petrol, 17 days of diesel and 27 days of total petroleum products.

And the problem for Australia is that they nearly all our fuel oils start as crude oil in the Gulf region before they go to Japan, South Korea, Singapore and Australia to be refined. If supply stops our reserves will barely last us for thirty days. After that everything, everything, not could stop, will stop! Think Venezuela.

I wrote last year about the alarming and strategically dangerous state of our national fuel oil reserves, in as much as we hardly have any. Bill Shorten the Leader of the Opposition in a recent speech told his audience that, “Right now, we have just 23 days of jet fuel, just 22 days of diesel and only 19 days of automotive gas.(petrol)” He added that when Prime Minister he would fix it. The Prime Minister, Scot Morrison, has not mentioned the problem, maybe he doesn’t want us to know?

Both of our would-be leaders are more interested in the show-time of denigrating each other and so winning the upcoming election — the security of the nation runs a distant second to getting their hands on the keys to The Lodge and even better, Kirribilli House.

Australians are seriously dependent on other countries for the food they eat every day. Most of that food arrives by sea. Any interruption to supplies would materially affect the diet of the nation to the point of hunger.

Australians are seriously dependent on other countries for the food they eat every day. Most of that food arrives by sea. Any interruption to supplies would materially affect the diet of the nation to the point of hunger.