![]() In 2018 the National Farmers’ Federation of Australia, set a goal for Australian agriculture to achieve production at the farm gate worth $100 billion by 2030. The production in 2018 was some $57 billion.

In 2018 the National Farmers’ Federation of Australia, set a goal for Australian agriculture to achieve production at the farm gate worth $100 billion by 2030. The production in 2018 was some $57 billion.

This is what I wrote for Episode 1 in The Global Farmer in December of last year:

That ($100 billion) is an increase of 66.6% on the production of 2018 or an annual increase of about 4%, and presumably, though they haven’t said as much, they all expect the producers to make a profit every year— which is more than they do now — but they don’t tell you that.

There are some truly grim truths about the financial ill-health of Australian agriculture and they are all produced by government statisticians and the Reserve Bank of Australia.

I then go on to dissect agriculture in Australia as it is now, warts and all. I look at debt levels and question whether they are sustainable. I note that as farms have got bigger, productivity has decreased and debt has increased. Skills are being lost at an alarming rate.

Cereal yield increases are not keeping up with inflation and the real value of wheat is declining and according to research in 2019 our producers have high costs and low yields when compared to other countries. Cereal farmers in the low yielding areas are having difficulty making a profit year on year; some if at all.

The statistics are blunt and uncompromising. They are the sort of numbers that not many producers like to recognise in public, but they are true and factual and researched by the profound Ben Rees, an Ag economist and farmer with over 50 years experience of agriculture and economics; Ben tells it as it is.

It would beneficial and help with understanding the perspective of this article which is Episode 2, to first read what I wrote in Episode 1 in December 2019.

This article may also at first glance seem to be at odds with what I have written recently, regarding the $18 billion, we are spending on imported food every year—but it isn’t, the reason being that what is discussed in this Episode is food which is surplus to our requirements in Australia, at least at the moment.

The population of Australia will increase by about 300,000 a year or 3 million by 2030 an increase of 12%. Unless production increases, exports will decrease as we feed more people and food imports will increase.

The Best Fresh Food in the World – Australia.

One of the fascinating features of Australian agriculture in the 21st Century is that we the people of Australia enjoy the best fresh food in the world. It is virtually all grown at home by Australian farmers.

One of the fascinating features of Australian agriculture in the 21st Century is that we the people of Australia enjoy the best fresh food in the world. It is virtually all grown at home by Australian farmers.

Our vegetables and fruits are clean and green and surpassed by none. Our meat, providing you know what you are buying, is as good as one can buy, anywhere in the world.

The exception is pig meat. If you buy fresh pork then you can be sure it is produced here in Australia. Virtually all other pig meats, bacon and ham included, are imported. Eighty per cent of the pig meat consumed in this country and valued at nearly $1 billion annually, is imported mainly from America, Canada, The Netherlands and Ireland.

Since the $100 billion target was set there has been a serious drought in many parts of Australia, the NFF may have changed the date for achieving their target, if they have I can’t find it in their literature.

So what are, or what were before the drought, the chances of the three main product groups in Australian agriculture, beef, sheep meat and wool and wheat making their contribution towards the whole of agriculture achieving an increase production from say $50 billion in 2018 to $100 billion at the farm gate by 2030?

My view is they have Buckley’s.

The Australian Beef Industry.

Many regions in the country are suffering or just experiencing the end of a series of major droughts.

Many regions in the country are suffering or just experiencing the end of a series of major droughts.

No sooner had they got out of the Millennial Drought than along came the GFC and then live export cattle fiasco that cost beef producers in the north a fortune.

Regardless of the drought, the Australian beef industry, as we shall see, will have to confront strong headwinds as it faces major competition in some of its most prized markets. It must do this and at the same time decide whether to accept the challenge thrown down by the NFF for it to increase its annual turnoff by 66.6% in ten years.

Some Statistics.

The Meat and Livestock Authority (MLA) were predicting the national herd would fall to just over 26 million head in 2019 and to climb back to 28 million by 2021-2022. Where it will go after that depends on how competitive we can be in the export market as beef consumption per head continues to decline in Australia.

The northern cattle industry relies heavily on the live export trade. Overall live cattle exports in 2019 totaled 1.3 million, for 2018 the total was 1,088,870, a strong, 26 percent above the 867,056 exported in 2017, but less than the previous three years, where in 2014 and 2015, about 1.3 million were exported. Can live cattle exports be increased by 4% year on year to 2030 to meet the new target?

Strong Competition .

Buffalo Beef from India and Beef from Brazil.

The live trade always seems a bit tenuous to me. Indonesia is our most attractive live market because of its proximity. A few days on a boat to that archipelago is far different to weeks to Israel and ten to twelve days to China and Vietnam.

Having said that Indonesia, against many predictions from Australia during the live export ban, is now importing ever increasing amounts of frozen buffalo meat from India and beef from South America.

The Indonesian market for Australia for both live, chilled and frozen beef is by no means secure. In August 2019 Beef Central announced that Indonesia had granted South American interests a 50,000 tonne quota for frozen beef. Australia in the fiscal year 2018/19 exported some 53,000 tonnes of the same product to Indonesia.

Again Beef Central reported in July 2019 that the National Logistics Agency in Indonesia, Bulog, was planning to import another 30,000 tons of  buffalo meat from India in 2019.

buffalo meat from India in 2019.

Imports of buffalo meat into Indonesia will continue to grow, nobody it seem knows how big the quota is that has been granted to India for 2020.

Beef Central and Reuters have mentioned it could be for 100,000 tonnes and that maybe 80,000 tonnes was imported in 2019. If that is the case then Indian Buffalo beef represents a significant challenge to the Australian beef industry in Indonesia.

The buffalo herd in India is about 97 million compared to the Australian beef herd of about 28 million. Between April and November 2019 India exported over 800,000 tones of Buffalo meat around the world, a major market for them is Vietnam. That figure was down 10% on the previous year, mainly due to China clamping down on illegal imports, coincidentally, mainly from Vietnam.

What quarantine measures are in place to ensure that foot and mouth disease is not introduced into Indonesia is far from clear, though it should be recognised that many states in India, and in Brazil for that matter, are foot and mouth disease free. Brazil claim that vaccination against foot and mouth disease is standard practice. Argentina makes similar claims.

The big challenge is that many in Australia predicted during the live cattle shipping ban that the Indonesians would not accept buffalo meat, now they are finding the reverse is true. It’s cheaper than beef and is in demand by the street food stalls.

There was a time when the justification for live exports from Australia was because there was a shortage of refrigeration in Indonesia would limit the market for frozen beef. It would appear that is no longer the case as they seem to be managing the increasing imports and distribution of frozen beef from India and Brazil without too much trouble.

Feeding cattle in a feed lot in Indonesia is tenuous in good times and downright awful in bad. Apart from the fodder that is grown locally there is a reliance on imported grains, at times this can place stress on the system.

In May last year Ross Ainsworth reported problems with a well known and log established feedlot in West Java. In December of the same year the ‘Farm Weekly’ reported problems ranging from animal welfare, drought and shortages of feed and water. Elders also sold their major share in a big feedlot.

Australian beef producers getting a poor deal.

One of the things that I find disturbing about both the live trade and the domestic slaughter is the question whether the Australian producer gets paid anything for the value of the offal and hides as well as the actual carcass weight for animals slaughtered in Australia.

There is a good article going back to 2016, where David Byard from the Australian Beef Association points up the difference between the carcass weights of identical steers, one slaughtered in the United States and another in Australia.

David claims that a 600kg live weight steer would yield 52% or 312kg in Australia and the same beast would yield 62% or 372kg in the United States. In the United States less is trimmed off the carcass before it is weighed and the producer in both countries owns the carcass until it is weighed.

David claims that a 600kg live weight steer would yield 52% or 312kg in Australia and the same beast would yield 62% or 372kg in the United States. In the United States less is trimmed off the carcass before it is weighed and the producer in both countries owns the carcass until it is weighed.

The processor, not the producer in Australia, gets the money for the 60kg they trim off the carcass before weighing.

That’s not the worst of it, the producer in America not only gets paid for the 60kg of trim, but they also get a percentage of the value of the offal.

In Australia, David still believes that Australian producers don’t get a penny for the offal because nobody in the meat trade can give him the formula that they use to calculate the amount they say they add to the value of the animal for the offal and hide at the time of purchase.

There is also a YouTube link which explains it far better than I can.

MLA reported in June of 2019: At current pricing, the potential value of beef offal is about $60 per head from a 275 kg steer, about $7.8 per head from sheep and about $8 from lamb. Exporters typically pack 18 to 24 items of beef offal and 5 to 9 items of sheep offal. Another 5 items of beef offal may be recovered from time-to time. Domestic producers supply about 7 to 8 items of beef and sheep offal.

On top of that is the hide value, which at present is at an all-time low of A$10 to A$20 for a good hide. Two years ago the same hide was making $80 to $100.

JBS, who have a 25% market share in the Australian meat processing sector made a global profit last year of over $9 billion. No doubt offal and hides contributed to that figure from their Australian operations.

The domestic kill is forecast at about 8 million, multiply that by $70 (offal and hide) and that is $480 million that doesn’t reach the producer’s pocket for cattle slaughtered in Australia. When the hide price was $100 that number grows to an impressive $1.28 billion.

When you add the value of offal and hides into the price of live cattle and it is easy to see who is getting a good deal.(prices are all over the place at the time of writing 4/20 due to the disruption of the global pandemic. Hides are worthless according to Bryant)

How can Australian cattle producers be world competitive while this kind of slight of hand is going on? If the NFF could fix this apparent anomaly they would be half a billion dollars or a billion dollars closer to their target of $100 billion.

Then again, I am reliably informed that when the question of producers being paid and identifiable amount for offal and hides is raised with the processors they are told, like David Byard relates, that the value of the offal and hides is built into the price paid for the animal. If you believe that then…

So, if the market to Indonesia is so close but somewhat tenuous and if this matter of the proximity of Indonesia to Australia is not an advantage, where is our next biggest potential market for beef? It’s China of course.

Beef to China.

This is from the publication ‘Rural Bank, Australian Agriculture 2017/18’.

Japan was Australia’s most valuable export market for beef at $2.1 billion, an increase of 10.8 per cent. Exports to Japan faced increased competition from growing US exports but benefited from an 11.6 per cent tariff advantage for frozen beef over the US which will continue to increase under the Japan Australia Economic Partnership Agreement and set to improve further under the Comprehensive and Progressive Trans Pacific Partnership.

Beef exports to the US increased by 14.4 per cent in value to $1.7 billion, following two years of decline. This was largely due to increased production in Australia and robust demand from US consumers. Despite being a large competitor, the US remains an important customer for Australian lean beef to compliment domestic production in manufacturing beef products.

South Korea was the only major market to import less beef from Australia in 2017/18, down 4 per cent to $1.2 billion. Exports came under pressure from increased US production which holds a 5.3 per cent tariff advantage over Australia.

China became a $1 billion market for Australian beef in 2017/18, with a 34.7 per cent increase in the volume of beef exported adding an extra $255 million in export value. Brazil remains the largest supplier of imported beef to China and is expected to continue to increase exports in 2018/19.

The take home message for me from all of that is that there is ever increasing competition for Australia in the world markets on which we depend as beef consumption continues to fall in Australia.

Brazil is now flexing its considerable muscle in the beef market in China. There has been an international reluctance to buy beef from Brazil and Argentina because of the scare of foot and mouth and mad cow disease. That will probably keep Brazil out of the markets in Japan and the United States which are so important to Australia. But it will not keep them out of China, where they have big ambitions.

Brazil is now flexing its considerable muscle in the beef market in China. There has been an international reluctance to buy beef from Brazil and Argentina because of the scare of foot and mouth and mad cow disease. That will probably keep Brazil out of the markets in Japan and the United States which are so important to Australia. But it will not keep them out of China, where they have big ambitions.

Australia must always remember that parts of Brazil are foot and mouth disease free and other areas have 100% vaccination programmes and these are gradually being accepted internationally.

Am I overplaying the march of Brazil into the world’s beef markets? I have a deal of respect for the USDA, here is the introduction of an article that everyone in the beef industry in Australia should read and will, quite frankly, find it a bit disconcerting. To start with I didn’t know there are 232 million cattle in Brazil (Aust 28 million) with the vast majority being grass fed:

In 2018, Brazil was the world’s largest exporter of beef, providing close to 20 percent of total global beef exports, outpacing India, the second-largest exporter, by 527,000 metric tons carcass weight equivalent (CWE). Moreover, USDA projects that Brazil will continue its export growth trajectory for the next decade, reaching 2.9 million metric tons, or 23 percent of the world’s total beef exports, by 2028.

JBS made a global profit last year of A$9.6 billion. JBS dominate the Australian meat processing sector with a market share of over 25%. Whether JBS Australia compete with JBS Brazil for the Indonesia market is unknown!

In early 2019 China stopped importing beef from Brazil following a ‘Mad Cow Disease’ scare. That ban was lifted in June 2019 and imports started up again. In 2018 China imported over 300,000 tonnes of beef from Brazil. Here in Australia we have to remember that Brazil has an enormous advantage over Australia because of the high processing costs in this country, which if we are to become internationally competitive must be addressed.

The average cost per head in 2018 excluding livestock purchases, incurred in processing beef in Australia was 24% higher than in the US, 50% higher than in Brazil and 75% higher than in Argentina. Australia’s costs are higher than those of all our major competitors in the beef markets.

Brazil’s ambitions are global. Mercosur is a trading bloc in South America comprising Brazil, Argentina, Paraguay and Uruguay. In July 2019 Brazil’s agriculture minister Tereza Cristina, a former director at the cattle-breeders association of Mato Grosso do Sul, on behalf of Mercosur, negotiated a deal to supply 99,000 tonnes of beef into the EU at a reduced tariff of 7.5%. Mercosur consider this to be a start but far less than the more than 300,000 tonnes they were seeking and they recognise that their quota represents only 1% of the EU annual beef consumption. “But it’s a start” she said.

Sheep & wool.

As for sheep and wool where we are going is anybody’s guess. It doesn’t seem that the national flock numbers are increasing, in fact they continue to decline as parts of the country are in a drought or trying to restock after drought.

As for sheep and wool where we are going is anybody’s guess. It doesn’t seem that the national flock numbers are increasing, in fact they continue to decline as parts of the country are in a drought or trying to restock after drought.

Looking at the graph the MLA are predicting a modest increase in sheep numbers from just over 60 million to just under 80 million in a couple of years. We shall see.

With good merino ewes selling at well over $100 per head, getting back into sheep is a big investment that will have to be supported by the banks. Even $62,500 for small flock of 250 ewe hoggets is a considerable investment in the future, double it for a decent flock and then it becoming serious.

I do wonder though, looking at the wheat yields in the lower rainfall areas, whether many of those farmers wouldn’t be better off being helped back into sheep and maybe goat production through a government financed restructuring initiative, rather than staying with the high-cost, sometimes profitable sometimes not profitable cropping regime, which is currently controlling them? Many are every year putting millions of dollarson the table and spinning the wheel on the weather.

Since 1991 sheep numbers in Australia have declined by 100 million. They have gone from 163 million to about 70 million in just under thirty years and during that period there has been an ever increasing world wide demand for sheep meat, especially lamb.

For many in WA , going back into sheep would mean replacing fences and watering points, not to mention shearing sheds if wool producing sheep are to be kept. This very good paper comparing cropping and sheep margins and profitability is well worth a read.

On a recent trip to the northern wheatbelt in Western Australia, I was horrified to see the changes. Fences have been ripped out so crops can be planted right up to the roadside, this means that there are no verges, no native bush and of course no wild flowers. Trees have gone to enable GPS to be employed. Not a sheep to be seen on some of the best merino country in Australia. Vandalism I call it.

I heard recently of a farmer in the West Australian wheat belt, now in his late sixties and having been persuaded some ten years ago by his son and heir to sell the sheep and go all cropping with a wheat, canola and lupin rotation, they had decided after a look at the balance sheet, they had made the wrong decision and it was time to spread the risk and get back into sheep.

Cutting a long story short, when the father had bought the foundation stock for their new flock, he realised that his son knew virtually nothing about sheep and the learning process, handing on his skills of sheep husbandry to the next generation, would have to begin straight away while time was on his side.

The same question arises, can the sheep industry from meat to wool increase its production by 66.6% in the next decade? That’s another 46 million sheep! That target defies all the predictions.

There is no doubt that the world wants red meat and lamb and mutton have a major place in that market. Whether we can restructure to meet these markets in the future remains to be seen.

Another possibility in the low rainfall areas are goats. There is still more goat meat eaten in the world than lamb and mutton. I have wondered for the last forty years why goats have never found favour with broad acre farmers. I suspect, like sheep, they look too much like hard work when GPS, tramlines an air conditioned cab, stereophonic sound, and the world wide web on the smart phone are the alternative.

The picture of the future does change whenwe look at wheat.

Wool.

It wouldn’t be a look at future agricultural production without looking at wool on it’s own.

It wouldn’t be a look at future agricultural production without looking at wool on it’s own.

Wool today represents just 1% of the world apparel market. What it was in the 1990s when the sheep population in Australia was at it’s highest I don’t know and it doesn’t really matter, because the likelihood of Australia ever getting back to those numbers, before Federal Agriculture Minister Kerin put his check book into his saddle bag and rode off into the night, leaving the industry as we knew it to perish, is remote to say the least.

In 1990 there were about 170 million sheep in Australia. In 2020 there are about 70 million and the numbers are forecast to decline. In that decline of 100 million some of the best merino genetics in the world were slaughtered, cut up, put in boxes and eaten, never to be replaced. That is a sin and a stain on Australian agriculture and on poor decision making in federal politics.

I remember saying to the then Minister for Agriculture in Western Australia, Monty House, shortly after the wool price crash that in my lifetime, unless he and his fellow ministers in other states talked some sense into John Kerin, the federal minister, and all the clowns in the wool bureaucracy, then merino wool would become a cottage industry. I’m still alive but the wool industry is not far off being consigned to cottage industry status,

The best and most honest book that has been written about the Australian wool industry collapse in 1991 was written by that well known, even famous wool grower, Charles Massey.

The book ‘Breaking the Sheep’s Back’ recalls how wool from the very beginning was the backbone of the Australian economy and provided the money for the foundation of this nation.

The wool industry in 1992 was chucked on the rubbish tip by the Hawke Labour Government after years of inept management. In the Introduction to the book Massey wrote:

The chain of events leading to the spectacular collapse of the Wool Corporation Reserve Price Scheme (RPS) had been repeatedly predicted (and in precise and accurate detail) since the 1920s by international observers and Australia’s best economic, business, academic and government department brains. These warnings gathered weight and momentum through each decade, reaching a crescendo in the years before 1991 collapse. Yet the warnings were to no avail. A group of government ministers, agri-politicians and wool industry and statutory leaders ignored the perspicacious and prophetic advice as they led the industry down the path towards calamity. Charles Massey ‘Breaking the Sheep’s Back.’

One of the sad things about the decline of the merino sheep industry in Australia is that we have lost the ‘wheat and sheep’ regions. Those areas are now just growing crops, cereals and canola mainly with a few lupins here and there.

A productive rotation of two or three years of clover pastures and sheep followed by a couple of years of crops took many years of research to finally determine which varieties suited which soil type and which rainfall zone .

When finally established a clover rotation proved so beneficial to the old and fragile soils in the traditional Australian wheat and sheep belt it will be remembered as a major milestone in the history of Australian agriculture.

For some of us who can remember the benefits of increased soil fertility and a reduction in the cost of cropping by putting a mob of sheep onto an abundant nitrogen generating clover pasture and getting the benefit in the next cropping phase of not only the nitrogen but the manuring on poor and for many of us virgin soils, the passing of the sheep industry is sad indeed.

Crop yields have not really increased over the last thirty years but weed problems and the resultant costs have. Considering our internationally low yields and poor potential for improvement I doubt the long-term sustainability of the cereal canola rotation.

Wheat into the Future.

It would seem that there is a better prospect for meat and perhaps wool production than there is for grain, especially wheat.

“While maintaining a continual focus on cost control and yield improvement remains a priority, the main message for the broader industry is that the high value grain price needs to be preserved to maintain competitive profitability, particularly for the lower yielding producers,”

‘Typical’ Australian farms with medium to low yields are unlikely to be sufficiently profitable at the average wheat price for the data set.”

Those are the views of Ashley Herbert a West Australian agronomist and Farm Adviser. I have often quoted this research, time has passed since it was done but the messages are as strong as ever and timeless. If anything the gap between Australia and its main competitors in the wheat market grows every year.

The average wheat yield per hectare in Australia is somewhere between 1.5 and 1.8 tonnes, depending on whom you believe. Whichever it is we lag way behind the world in what we have been able to achieve in yield increases over the last thirty years.

In my Global Farmer article of March last year where I predicted ‘There will be no Australian wheat industry in 23 years time’. I noted that some are forecasting that Australian wheat yields will decline from the internationally uncompetitive position they hold at present. I also point to an interactive map of world wheat yields by country over time, have a look and play around the Baltic and Russia and you will see what I mean.

I wrote at the time: It’s one of those sites that can settle a disagreement on where world agriculture is going and where it has been. Just to make my point about the failure of Australia to keep up with the rest of the world on improving wheat yields, this is what has happened to wheat yields between 1961 and 2014 in some of the main wheat growing countries, all in tonnes per hectare plus a percentage increase.

USA 1.68 to 2.94 = 75%; UK 4.3 to 8.6=100%; Russia .99 to 2.01=152%; Brazil .53 to 2.75=418%; India .89 to 3.15=253%, in Australia the gain has been from 1.13 to 2.01=78%. Ukraine .99 to 4.01=304%; Belaraus .99 to 3.9=303%; Romania 1.33 to 3.6=170% and so it goes on.

The data on this site gives a wheat yield per hectare in Australia 20 years ago at 1.9 tonnes, the same as today, ABARE and others put it a bit lower at 1.8 tonnes.This means that the average, stress average yield has moved little in 20 years.

It is worth remembering when considering the cost to grow crops in Australia that virtually all of the inputs are now imported. Machinery is one of the main costs and anyone who has studied the machinery market in the EU and in America knows full well that we don’t have the cheapest deals.

Another high cost complication is the necessity to employ the services of the distributors to repair tractors and headers. This business of having warranties and parts all tied into computer diagnostics might be alright in the EU or in the close cropped area of America, but in Australia where a trip of a hundred kilometers of more might be involved for a short stay on site is an expensive nonsense. I spoke to someone recently who paid over $100/hour plus mileage for a twenty minute job on site. The distributor was over 3 hours away.

There is no point in asking whether we can increase wheat yields by 66.6% because we know we can’t. Nobody believes we can. All we can hope for is an increase in price. But then again one of Australia’s leading commentators Malcolm Bartholomaeus recently told the ABC that based on our wheat exports at around 10 to 15 million tonnes:

“On those global figures, we produce 2.7 per cent of the global crop and account for 6.8 per cent of the global trade,” Mr Bartholomaeus said.

“We are almost irrelevant at this particular point in time in terms of that global wheat market.”

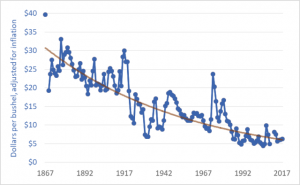

Further more the real price of wheat has been falling for over a hundred years. Any prediction that the real price will increase needs to be accompanied by a bucket of salt.

Researchers at CSIRO are claiming that wheat yields in Australia have remained the same between 1990 and 2015, but more seriously they are further claiming that potential yields have declined from 4.4 tonnes per hectare to 3.2 tonnes per hectare during the same period.

They describe the potential yield thus: Potential yields are the limit on what a wheat field can produce. This is determined by weather, soil type, the genetic potential of the best adapted wheat varieties and sustainable best practice. Farmers’ actual yields are further restricted by economic considerations, attitude to risk, knowledge and other socio-economic factors.

While yield potential has declined overall, the trend has not been evenly distributed. While some areas have not suffered any decline, others have declined by up to 100kg per hectare each year.

Have a look at the map to see what they claim for your area. Rainfall patterns are shifting. Without getting into the climate change debate we know here in WA that there has been a marked shift in rainfall patterns as they have moved from the north eat to the south west.

Down on the south coast from Albany and the Great Southern to Esperance cropping is now a major part of the regional agriculture, planting takes place at the same time as Geraldton 1000km to the north. Fifty years ago much of the Great Southern was too wet and planting in Esperance was at least two months after the wheat belt.

The Global Wheat Market is Changing.

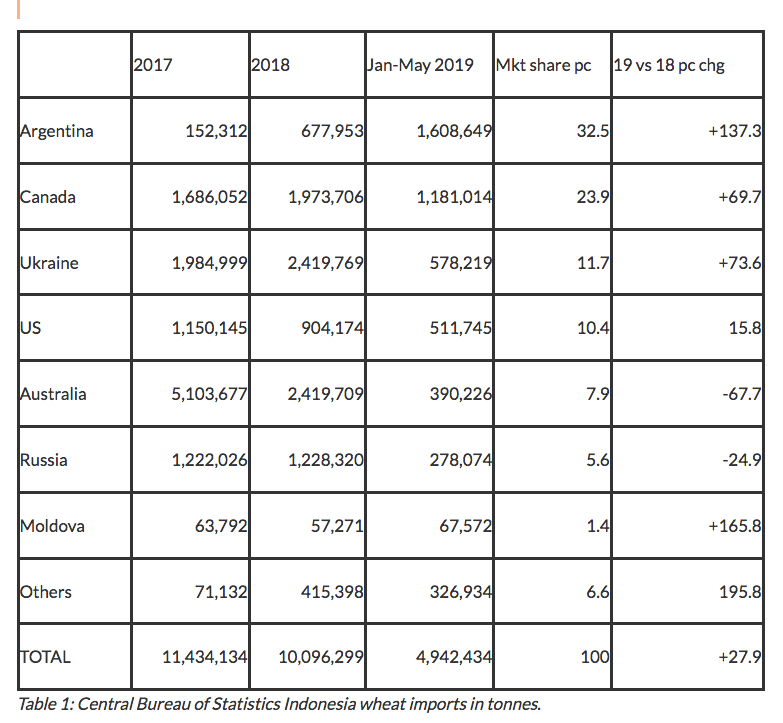

That point is driven home when we look at the changes taking place in the market for wheat in of all places, Indonesia. Now, all the market theorists will tell you that the proximity to a bulk market like the wheat market in Indonesia, there has to be an advantage in freight costs.

Indonesia, or at least those supplying the Indonesian market think otherwise. They are putting their hands in their pockets to build their exports of wheat in what will soon be the biggest wheat market in the world.

There are 153 million millennials in Indonesia that is people born between 1980 and 2000 and they dominate the market. Their incomes are growing and they are demanding the best of everything and that includes food.

This table was originally published in a Grain Central article earlier this year. For those who think we are home and hosed being so close to Indonesia that we can almost touch them – have another look:

That is a very worrying table and I am almost certain that few farmers, especially in Western Australia where most of our export wheat is produced, are aware of how much market share we have lost in Indonesia and how our proximity, just a few days by boat, is no longer an advantage.

The WA farmer owned cooperative CBH, in an attempt to secure a market in Indonesia invested heavily in flour milling with little success, in fact the mills have needed extra capital, WA shareholders money, to keep them out of trouble.

Nice series of posts and an impressive blog. Came across your site about a month ago when I decided to try and learn a bit more about ag especially regarding its politics and economics. I particularly appreciate the recommendation of Ben Rees – I had never heard of him and have since been going through his reports and presentations. I saw one of his documents was as recent as 2019. Are you aware if he would he still take enquiries regarding his work? Keep up the good posting!

Regards,

Daniel

I will send Ben your email and then it is up to him. I think it will be OK. Thanks for the comment.

Regards

Roger

Appreciate it. Am not sure whether I will contact him or not but I’m working on a political/economic essay about the stuff going on in the MDBA, and am trying to get my head around the finer details of the economics. Some of the ABARES accounting I find devilishly hard to track (I don’t really have a background in economics – but am strong in maths – and just work on the family farm in Southern NSW but everyone round here is becoming increasingly political and I’m beginning to think most of them are probably heading down the wrong path). If I am satisfied that I can I understand the economics myself I’d prefer to leave Mr Rees in peace – he must be getting on a bit in age! Also, forgot to mention that I thought a piece I read a while back on the Cronin Family was enlightening. I have read some stuff about banking by Evan Jones in the past but I never understood the extraordinary role of external players like Ferrier Hogdson until I read your blog.

Thank you for responding to my previous comment.

Kind regards,

Daniel

I have just come across your blog via John Fairfax. I am impressed by the your choice of topics and the effort you put into research. As I come from the land and once was employed by Qld Country Life, I am interested in this country’s agriculture and its future, which don’t look very promising, as you say. The plight of the farming sector has been ignored by politicians from John Kerin onwards as you say and even the former Deputy Prime Minister John Anderson, a farmer himself, was unable to stop the slide.

Thanks Kate, agriculture does have its problems and they seem to be getting worse. Thank you for your comments and I do agree.