The last paragraph in Ben’s paper, which questions the legality of MPCI, should cause the promoters of MPCI to at least ponder and then ponder again. Particularly Mr Tehan.

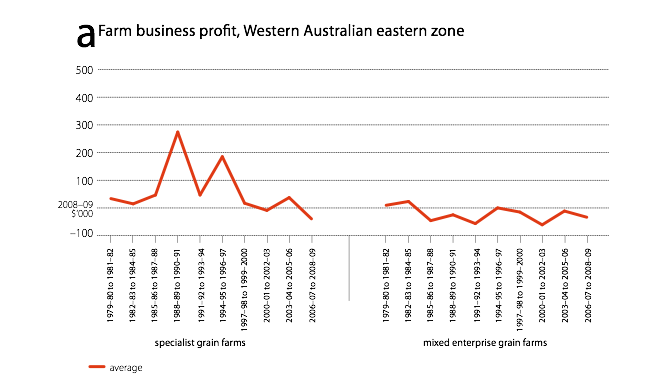

There is interest and support in high places of government for MPCI. Has MPCI been politicised to gain support among the electorate without the proponents explaining the cost? Certainly this graph is a few years old but the trend line is obvious, maybe if it has changed direction you will let me know? By that I mean whether there is sufficient above the line to afford MPCI.

Graph ABARES

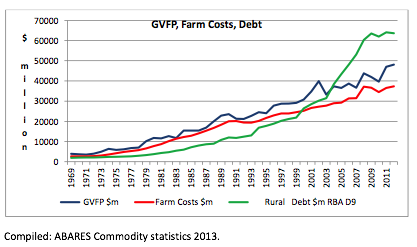

Graph ABARES

You can read how deeply concerned Ben is about agriculture and particularly the drought situation in Queensland and NSW by going to:

Roger Crook

Roger,

The Senate Economics Legislative asked me a question on notice at the Inquiry on March 18th. The question was to compile a short note on multi peril crop insurance. It appears that the House Economics Committee led by Dan Tehan from Victorian Western Districts is pushing it. Also the policy panacea White paper will recommend it.

This attached note was subsequently submitted and accepted by the Senate Economics legislative Committee. It should have been incorporated in Hansard. I do not know if you can publish; but, at least you know it is being pushed at high levels.

cheers

Ben

I have checked and it is legal to publish, as it has been published by the Parliament of Australia.(Editor)

Question on Notice: Senate Economics Committee Legislative Committee 18/3/2015

Short Note Multiperil Crop Insurance

Ben Rees ; B. Econ.; M. Litt. (econ.)

Crop insurance is an allowable excludable agricultural support program under WTO Agreement on Agriculture (AoA). Crop insurance is a feature of agricultural policy across: USA, Japan, Sweden, Canada, France, Spain, Mexico, Korea. The most comprehensive program is now in operation in the USA. This probably is the example that needs to be explored

Multi crop insurance has been part of US agriculture since 1938 and is funded under the US Farm Bill. In the 2014 Farm Bill, there was a move away from A.o.A Decoupled Income Support (deficiency payment programs) to greater emphasis on multi crop insurance. Multi crop insurance was expanded to include most commercial crops grown in the USA.

From 2008 , interest broadened from crops to livestock. This has led to policies that cover Loss of Gross Margins ( LGM) calculated as market value less feed costs . Livestock covered are: cattle, dairy, swine. Livestock Risk Protection policies (LRP) provide against price decline.

F.C.I.C.

Federal Government involvement is delivered through the USDA’s statutory authority, Federal Crop Insurance Corporation (FCIC). The FCIC provides a subsidised reinsurance facility for private sector insurance providers. Standard Reinsurance Agreements (SRA) establishes terms and conditions for payment of subsidies on reinsurance contracts. Livestock Price Reinsurance Agreement (LPRA) is the livestock reinsurance agreement between the FCIC and private sector insurers.

The role of the FCIC is to promote economic stability of agriculture through a system of crop insurance and research and development of insurance products. The FCIC also pays subsidies to farmers to reduce premium costs. Farmer subsidy is 65% of premium for established farmers. For beginning farmers, there is an additional 10% above established farmer premium subsidy.

RMA

Underneath the FCIC sits the Risk Management Authority whose role is to support and regulate risk management.

Australian Situation

In Australia crop insurance has been on offer since 1918. It is less sophisticated and mostly involves risk management of single risk events such as hail. Recent interest has emerged in multi crop insurance. As it is not supported by public subsidies, little interest can be expected in this area by private insurers. The NSW Government commissioned a report that relied upon Reports provided by NRAC and ABARES. NSWFF has been supportive of this research

Some private research has been done also in Queensland by individual growers such as Mr. Rodney Hamilton of Callitris , Condamine. Reliance upon private insurance providers makes multi peril crop insurance very costly.

Comment

Given the high cost component of Australian farming, private sector high cost risk management programs would seem a highly optimistic policy approach. Government support must be considered if this option is to be developed in any future policy change of direction.

Criticisms of US multi crop insurance abound . Potential for corruption throughout the system is a concern. Large farmers do well whilst smaller operations continue to struggle. Another criticism is that in the past it has been very expensive to taxpayers.

Extension of this support system in the 2014 farm bill is as yet unproven in terms of cost to taxpayers and effective support to rural America. The disregard for WTO A.oA. Rules which stipulate income only support ( Refer Annex 1) is concerning for international agricultural policy. Australia might need to ponder the signing of international agreements under the External Affairs Power ( Section 51 xxix) that implicitly alter without referenda the intent, extent, and power of other sections of the Australian Constitution such as Sections 90; 91; Section 51 (xx).

References: various USDA web sites

Livestock

www.rma.usda.gov/livestock

Reinsurance Agreements Overview

www.rma.usda/pubs/ra/

2015 Crop Policies and Pilots

www.rma.usda.gov/policies/2015policy.html

Annex 1

Important Section of Annex 2 are Sections 7 and 8;

Section 7

Section 7 covers financial participation by Governments in income insurance and income safety net support programs.

Subsection (a)Agriculture must comprise at least 30% of an enterprise operation

7 (c) The amount of such payments shall relate solely to income; it shall not relate to the type or volume of production (including livestock units) undertaken by the producer; or, to prices domestic or international, applying to such production; or to factors of production employed

Section 8

Section 8 provides for relief from natural disasters ( made either directly or by way of government financial participation in crop insurance schemes)

. (a) Eligibility for such payments arise only following a formal recognition by government authorities that a natural or like disaster has occurred or is occurring ( covers disease, pest infestations, nuclear accidents, or war on Member. Production loss must exceed 30% of production average over previous 3 years or three year average over preceding past 5 years

. (b) Payments apply only to losses of income, livestock,, land or other factors of production due to declared natural disaster

Attribution: Parliament of Australia – Common Licence

Multi-peril crop insurance seems a great idea – at least in theory. However the feasibility has been repeatedly denied by studies. Government assistance could kick-start schemes, but will inevitably create an imbalance. Economists call this “adverse selection” – even subsidized schemes would be adopted more for high risk situations.

To attempt to counter adverse selection, the promoters of schemes would screen applicants. Apparently the current fee for screening is a one-off of some $5000 for Western Australian farmers. Results of this screening would determine insurance premiums. However it is doubtful whether this screening could eliminate “moral hazard”, and it is fascinating to imagine the loopholes that could be engineered by farmers and their advisers. You could be sure however that the insurance companies, like the bookies, would not be out-of-pocket.

Meanwhile, opportunities for more substantial improvement in farm profitability are seemingly over-looked. Productivity improvement stalled some decades ago (ABARES data), with water use efficiency usually only 60 to 70 per cent. Yet most people know of examples of 90 per cent or more being achieved. A more worthwhile policy question is – why is this potential not being achieved, now over a period of several decades?