Persistence.

The stand out feature following the publication of ‘National Bank Bastardry’ in the last issue of the ‘Global Farmer’ was the number of people, including those on Facebook, who encouraged us to keep on going with the story and wished the Cronin family all the best for Christmas and especially for a better New Year. Many identified with the Cronin’s problems, some related ‘tough’ experiences with their bank and as a result, did not want to go public with either their name or their story, except to say they had one. That is not a healthy relationship between borrower and lender – between the farmers and their banks. For every Charlie Phillott in Queensland and Cronin family in Western Australia, it appears there are many others with similar stories, which will never be told.

Smoke Screens and Threats.

Harold Cronin wrote to Ferrier Hodgson (FH), appointed by the National Australia Bank (NAB) as the receiver managers and manager for the mortgagee in possession of what was formerly Chambejo Farms, the Cronin family farming business. He asked for a copy of all (two or three) the valuations on Chambejo Farms that FH had commissioned from a firm of valuers, Opteon, and for which Chambejo Farms had paid. Harold wrote based on this advice:

- The Corporations Act obliges receivers to keep financial records that “correctly record and explain” transactions they enter into while they are controlling a company. Directors and shareholders of the company have the right to inspect those records. These provisions appear in section 421 of the Act.

What follows is the body of the letter he got back from FH. It appears to be the very antithesis of section 421 0f the Corporations Act. If you don’t want to read the whole letter here is a short review, you should read the letter, because it’s a blinder:

FH wrote back to Harold and stated that they couldn’t release the information he requested because they, FH, had signed an agreement with Opteon invoking the Privacy Act 1988. Their contention was and is that the results of the valuations, paid for by Chambejo Farms as mortgagor are secret and unavailable to Chambejo Farms unless they signed an agreement, which absolved Opteon and FH from any action or proceedings based on the valuations. Even if they signed, it only meant that FH and Opteon would further consider the request; in effect they could still say no. It’s true – FH and Opteon wanted Harold and his family and their Trustee in Bankruptcy to give them an escape from possible prosecution. Why would they do that? It’s obvious isn’t it?

Here is full text of the letter from FH to Harold Cronin and his Trustee in Bankruptcy – and it’s unbelievable:

We refer to Mr Harold Cronin’s letter received by us on 17 November 2015 (a copy of which is enclosed with this letter for ease of reference).

1. You recently asked us to provide a copy of valuations we obtained for the Chambejo Group during the course of our appointment as agents for the mortgagee in possession and receivers of managers of the Chambejo Group or its properties. Specifically , the valuation reports referred to are the two valuation reports for “Home”, “Max’s”, “Lee’s”, “Piercy’s”, “Johnny’s” and “Malkana”,West River/Ravensthorpe WA 6346 on 21 November 2013; “Home”, “Max’s”, “Lee’s” and “Malkana”,West River/Ravensthorpe Western Australia 6346 on 11 August 2014 only (collectively, the Valuation Reports).

2. The Valuation Reports are subject to confidentiality provisions and Privacy Act 1988 restrictions which means we must ask for consent of the valuers, Opteon (Western Australia) Pty Ltd (Opteon), to disclose them to you. Without that consent, we will be breaching our arrangements with Opteon.

Non-reliance3. In order to obtain access to the Valuation Reports, you must agree not to rely upon the Valuation Reports, in any respect, and especially for the purpose of commencing proceedings against Opteon. (Emphasis added Ed.)

4. This includes (among other things) reliance upon the content of the Valuation Reports, the circumstances in which the Valuation Reports were obtained, and the circumstances in which the Valuation Reports are now released.

5. In addition you agree to release and hold Opteon and Opteon Property Group (OPG) harmless from all actions, suits, proceedings, accounts , complaints (whether to the Valuers Registration Board or any other entity), claims, demands, costs, expenses and damages. You discharge OPG and Opteon from all or any liability whatsoever , whether pursuant to contract, tort, statute, or otherwise, which but for the execution of this Deed Poll you now have or had at any time previously or might have in the future arising out of or in connection with all matters relating to the Valuation Reports or any other valuation by Opteon, whether such actions, suits, proceedings, accounts, complaints, claims, demands, costs, expenses and damages be direct, indirect or consequential or past, present or future or certain, contingent , ascertained or not ascertained and whether for monies claimed as aforesaid or not or pursuant to or arising out of the Valuation Reports or otherwise to the intent that all questions and issues which might but for this Deed Poll arise and any time shall be finally settled and you will indemnify OPG and Opteon and keep OPG and Opteon indemnified each other in respect thereof. (Emphasis added)

6. You indemnify and must keep OPG and Opteon indemnified against any actions, suits, proceedings, accounts , complaints, claims, demands , costs, expenses or damages, and against any and all liability whatsoever, whether arising at law or in equity, and whether pursuant to contract, tort, statute or otherwise, that OPG and Opteon may incur as a result of the Valuation Reports or as a result of you complaining verbally or in writing to any industry body or any current or potential client or court, whether such actions, suits, proceedings, accounts, complaints, claims, demands, costs, expenses and damages be direct, indirect or consequential or past, present or future or certain, contingent, ascertained or not ascertained and whether for monies claimed as aforesaid or not or pursuant to or arising out of the Valuation Reports, your complaints or otherwise.

7. You acknowledge that valuation reports are only valid for 90 days from the date of valuation. As the Valuation Reports are being released to you well outside of this time period, you acknowledge and agree that you, or any persons whom may have any direct or indirect interest in the properties valued, cannot rely of the Valuation Reports.

Confidentiality.

8. You agree that all information exchanged by Opteon, Ferrier Hodgson, nab and the Chambejo Group in respect of the valuations is confidential and contains personal information of the valuers and you must not disclose the valuations to any person without the prior written consent of all other parties (namely Opteon, Ferrier Hodgson and nab).

9. You agree that in consideration for Opteon and Ferrier Hodgson and nab disclosing the valuations, you promise to maintain the confidentiality of the valuations.

10. You agree that clauses 8 and 9 remain binding upon the parties, except in the following circumstances where prior notice of the disclosure is given to Opteon and Ferrier Hodgson:

a. where the valuations are disclosed to a party’s accountants, insurers or legal advisers in connection with legal proceedings;

b. where the valuations are disclosed to the Australian Taxation Office or any other public authority to the extent and for purposes required by law; or

c. where the valuations are required to be disclosed by law.

Moving forward

11. Please sign (in front of a witness, who must also sign) and return one copy of this letter. Please keep the other for your records.

12. Once we receive an original, signed copy of this letter from you, we will provide it to Opteon to enable its further consideration of your request.

Yours faithfully

Darren Weaver.

Correct me if I am wrong, I mean that, tell me if I am wrong – because but it appears to me:

- Ferrier Hodgson and Opteon have entered into an agreement based on the Privacy Act 1988. That agreement enshrines matters concerning the valuations on Chambejo Farms, which Ferrier Hodgson and Opteon have agreed to keep secret between themselves and have signed an agreement to that effect.

- As a condition to releasing that information to Harold Cronin, Ferrier Hodgson and Opteon require the Cronin family and their Trustee in Bankruptcy to sign what amounts to a secrecy agreement. That agreement as detailed above would absolve Opteon and FH from any action or proceedings that might result from the valuation reports written by Opteon and accepted by Ferrier Hodgson. There appears to be some contradiction between Clause 5 and Clauses 8,9 and 10 (a) (b) and (c). However the intent seems clear as does the motive for requiring such a document to be signed.

- Essentially they are saying, are they not, that there is information in the reports that may be actionable and from which, they want absolving, yet in another part of the agreement, Clause 10, a,b and c, this requirement seems to be at variance Clause 5. Is that legal? If an offence has been committed against the Corporations Act or on Common Law ruling of duty of care, can one be bound by an agreement to keep an offence secret? Which Clause takes precedent over the other?

If you pay for it, do you own it?

There is then the matter of ownership of the valuations. The mortgagor, Chambejo Farms, through their agents the receiver manager, FH, paid for the valuations. If the agent of the mortgagor, FH, enters into an agreement with a third party, in this case Opteon, does that not mean that the mortgagor is automatically party to that agreement? Presumably the mortgagor paid the legal costs incurred in the drafting of the agreement between Opteon and Ferrier Hodgson – so why the secrecy? Can these people just ignore section 412 of the Corporations Act? (see Smoke Screens and Threats, above).

Harold Cronin wrote straight back to FH and very bluntly told them he wouldn’t sign the agreement. He has no idea what their Trustee in Bankruptcy did.

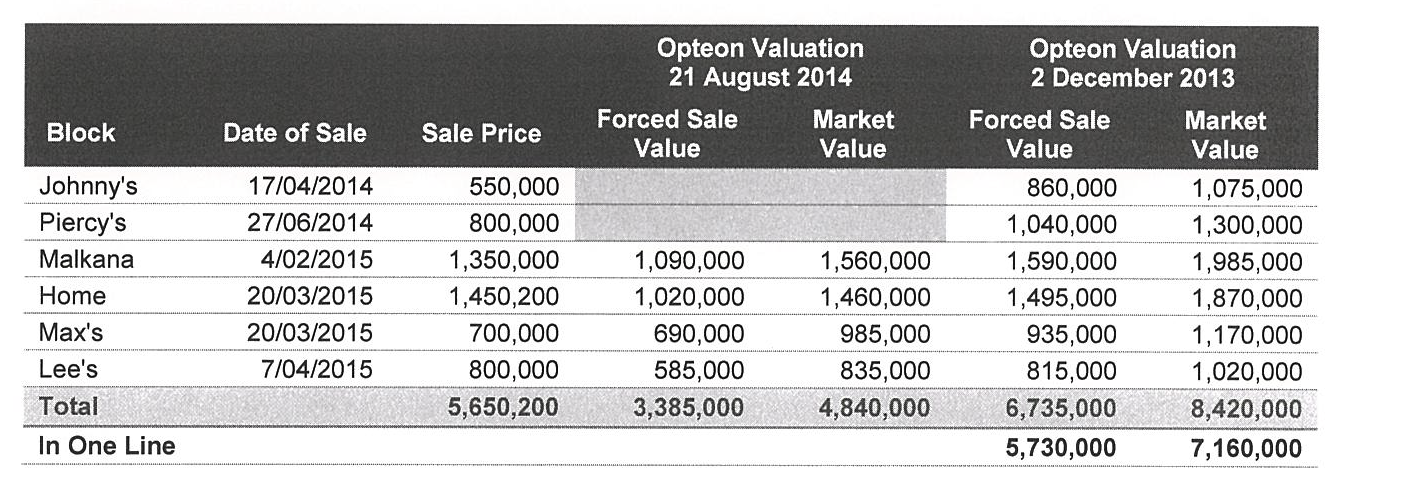

Having refused to sign the agreement, quite unexpectedly, on December 31 2015, the Cronin family received the following valuations from FH (Table 1). We have no idea why FH changed their mind and provided a minimum amount of information on valuations, sale prices achieved and what they claim was the marketing costs they approved for the disposal of Chambejo farms. Looking at the prices received for the six properties – one can only conclude that the advertising/marketing cost at $33,214 was a failure and a waste of money and that the agents were overpaid and poorly managed.

Just to refresh your memory. The NAB cut off all funds to Chambejo Farms and to the Cronins as individuals in January 2013. The receiver managers were appointed on May 4 2013. It was not until December 2013, over six months after they had been appointed that FH commissioned the first valuation, why did they wait so long?

You will also notice from Table 1 that it was not until 2015 that the majority of the Chambejo Farms were sold. FH had the properties re-valued in August 2014 and the valuer reduced the value of all the unsold properties. Why did they do that?

In the first episode (NAB Bastardry) several legal opinions quoted the law of this land and showed us that the mortgagee must not sell more of the mortgagors property than is required to satisfy the mortgagors debt. In other words it is open to question in this case whether the receiver needed to sell all of Chambejo Farms. Based on the valuations below it would seem that FH and the NAB overstepped the law when they seized all six farms. That’s not half of it either, as you will see.

The Valuations.

Table 1

Table 2

We now need to look at whether the Cronin family received a fair price for their farms. It remains unexplained by the receiver manager, Ferrier Hodgson (FH), why Opteon were of the view that the Chambejo Farms decreased in value by $1.2 million between August 2013 and December 2014. What was the evidence, the reason for this decrease in value?

Invaluable Independent Valuation and Advice.

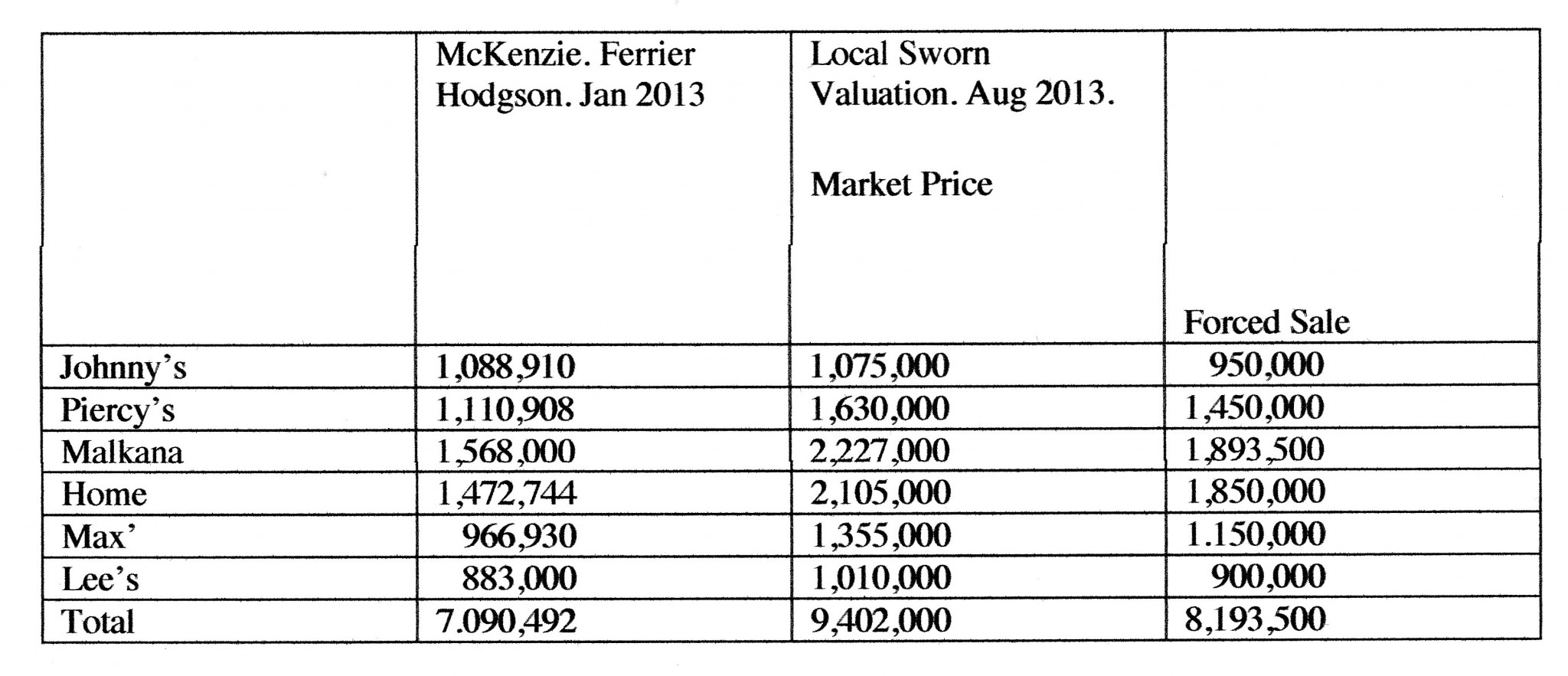

The independent valuer appointed by the Cronins (Chambejo Valuation) researched the prices paid for land sold in the same district as Chambejo Farms in 2011, 2012 and 2013. At least thirteen (13) properties were sold in the same ‘district’ as Chambejo Farms. What is evident, contrary to stories we have heard, land sales slowed during the period but values were maintained, they did not go down. For example the following prices were received in the Chambejo district: Dec 2013 approx 4 km east of Johnny’s, no infrastructure, Clark to Beli $1040/ha. In 2015 the block next door to the ‘Home’ block sold for $1306/ha in a deal between Dudlee and Mickleton. Twenty kilometers north east of Johnny’s block, Tink to Chambers for $1296/ha and so it goes, there are so many more and none even close to $550 a hectare.

What the independent valuer did when compiling the ‘Chambejo Valuation’, was the approved method of valuing a property. In his report the valuer has also detailed all the improvements on the various farms and where necessary, like a house, commented on the condition they were in at valuation. So we have a record, set in stone as it were, of the condition of the Chambejo Farms in August 2013. It must be remembered that the NAB became the De facto manager of Chambejo in January 2013 and FH the receiver managers etc, in May 2013.

Fair Market Value – Duty of Care.

What is a ‘fair market value’? As you will read below the Financial Ombudsman Service (FOS) has developed a very strong opinion on ‘fair market value’ based on the law of this land.

Before we look at the opinion of the FOS, look again at the price Ferrier Hodgson ‘achieved’ when they sold Johnny’s block. The Opteon market value in December 2013 was $1,075,000, the same value as the independent valuer put on the property in August 2013. It was sold in April 2014 for just $550,000, 51% of not one, but of two sworn valuations. How on earth can there be any justice in that? Is that a fair market value based on the definition as determined by the courts? How can anyone explain $550,000 as market value on a $1 million property and at one and the same time claim they have shown duty of care to the Cronin family? Piercy’s sold for $800,000, again for 50% of the independent valuation. Unbelievable!

Both Opteon and the local independent valuer put the same value on Johnny’s. Both valuers have also submitted a market price and a forced sale price. But as you will see below under the heading ‘Market Value’, the law does not accept a ‘forced sale value’ as being the true value of the property. The law is unequivocal – there is no such thing as a ‘forced sale valuation’ – it’s not legal – you can’t have two values on a property, only one – that’s the law. How many properties have been sold for a ‘forced sale value’? How many mortgagees know this and more importantly knew this at the time of sale.

The Cronins had a debt of about $6 million at the time the NAB manufactured a default and then appointed FH as receiver managers and managers for the mortgagee in possession. Based on the independent valuation of $9.4 million and the now flawed valuation of Opteon of $8.4 million, the NAB had no right to seize all six of the Chambejo Farms. The difference between the Cronin debt and the independent valuation of their farms was about $3.4 million. Had sufficient farms been sold to meet the debt, the Cronin family would have finished up with land assets of about $3.4 million, their machinery valued at close to $2 million and everything else that would have enabled them to keep farming would have been intact.

According to Michael Galvin QC, quoting from a case of MBF Investments V Nolan, Galvin gave the opinion that should a receiver manager sell more assets than were required to satisfy the debt then: ‘Such behaviour would be an unconscionable exercise of the mortgagee’s power of sale’. He was supported by Ms Roberts of Lavan Legal, who also reminded us of the common law duty of good faith. To challenge whether an act has been an ‘unconscionable exercise’ needs money for lawyers – as does entering into the maze of the common law and questioning whether the ‘duty of good faith’ has been applied. No money and unconscionable exercises continue and good faith becomes ecclesiastical.The poor have no advocate in matters of law.

That means it is open to question whether the NAB and FH had the legal right to sell all six Chambejo farms?

It also means that the Opteon valuations do not stand up to rigourous examination because while other properties were selling, (as detailed in the independent valuers report) Ferrier Hodgson, maybe because potential buyers knew they were selling on behalf of the mortgagee, could not achieve market value for Chambejo Farms. Then, and we don’t know why, 8 months later Opteon reduced the value of the Chambejo Farms. Did they do this of their own volition, if yes, why? The problem that Opteon has and by default FH has, is that they now have to prove that the reduction in Opteon’s valuation of Chambejo Farms reflected a change in ‘market value’ between August 2013 and December 2014.

If Ferrier Hodgson based their eventual selling price on what Opteon called a ‘Forced Sale Value’ then they have a problem, because there is no such thing as a ‘forced sale value’.

Market value – This is the view of the Financial Ombudsman Service. Bulletin No 38.

The concept of market value is crucial to the assessment of claims in Queensland and under the Corporations Act. As discussed earlier, in Victoria and Tasmania regard is to be had to whether the mortgagee obtained the “best price possible” but this term can be read as being equivalent to market value.

The starting point for describing market value comes from the decision of Griffith CJ in Spencer v The Commonwealth as follows:

“In my judgement the test of value of land is to be determined, not by enquiring what price a man desiring to sell could actually have obtained for it on a given day, i.e., whether there was in fact on that day a willing buyer, but by enquiring ‘What would a man desiring to buy the land have had to pay for it on that day to a vendor willing to sell it for a fair price but not desirous to sell?” 13 (emphasis added)

While it is not by any means usual for a vendor to be “not desirous to sell”, we understand that what is meant is that there are no surrounding circumstances or pressures which could result in the acceptance of anything less than a fair price.

In Queensland it has been said that it is not necessary to show that an actual purchaser would have paid more but it is necessary to show that the price obtained was less than market value as determined by having regard to expert and other relevant evidence.14 In our view this approach can be applied to claims under the common law and that other statutory provisions.

The Australian Property Institute has issued a guidance note dealing with the mortgage industry and has adopted the International Assets Valuation Standards Committee definition of market value which it sees as paraphrasing the definition in Spencer.15 Market value is defined as:

“ . . . the estimated amount for which an asset should exchange on the date of valuation between a willing buyer and a willing seller in an arms’ length transaction after proper marketing wherein the parties had each acted knowledgeably, prudently, and without compulsion.”

The term market value does not include the concept of a forced sale value and so a figure based on a forced sale would not be regarded as the correct measure.16 While it may be correct to say that the mortgagee was forced in a practical sense to sell the property, that does not mean it is only entitled to obtain the forced sale value which may be included in a valuation.

Essentially the reason why a forced sale value is not an appropriate measure of the value of a property is because the law requires that the mortgagee obtain market value and not a forced sale value. In our view a mortgagee ought not to have regard to a forced sale value when determining a reserve or listing price or when assessing an offer. For the same reasons ABIO (Australian Banking Industry Ombudsman. Ed) will not have regard to forced sale values when assessing cases.

In some cases it may be necessary for ABIO to engage a valuer to give an expert retrospective opinion on the market value of a property. For example, if advertising is so inadequate that we cannot be satisfied that the property was put to the market and the valuation material available is not clear or adequate, an independent and retrospective valuation may be required.

Is breaking the Law legal?

- Did the NAB conform with the law when they seized all six of Chambejo Farms properties when the sale of some, not all, would have settled the debt?

- Did Ferrier Hodgson refer to or use ‘Forced Sale Value’ when negotiating the eventual sale of the six Chambejo Farms?

- What does it say for the character, the quality of the mateship of the purchasers of the Chambejo Farms when they purchased a neighbours land for half its value, in the full and certain knowledge that it was a ‘mortgagees sale’? They must have known that all they were doing by paying that price was putting their fellow farmer deeper into the merde.

- Do all of those landholders who have, over time, been placed in the hands of a receiver manager and seen their property sold for a ‘Forced Sale Value’, now have some redress against the receiver managers and their mortgagee? It’s a question that must be answered by the regulators – but who are they? Do they Care?

There is no way that the sale price of $5.6 million achieved by FH for the six Chambejo Farms’ properties valued by two valuers at between $8.4 million and $9.4 million can considered as being ‘fair market value’ as defined by the Financial Ombudsman Service (FOS), the Australian Banking Industry Ombudsman (ABIO) and the Assets Valuation Standards Committee of the Australian Property Institute and not forgetting, Griffith CJ in Spencer v Commonwealth.

Bureaucratic incompetence at the big end of town has won again and apparently it goes unquestioned by the regulators. Who is it that has the power to say to Ferrier Hodgson and the National Australia Bank ‘please explain’?

Ferrier Hodgson have offered no explanation as to why after nearly three years of doing we know not what, but obviously not much, they were only able to achieve $5.6 million for an estate which, originally, their own valuer had priced at $8.4 million and an independent valuer had priced at $9.4 million.

Who is it that asks Opteon why they reduced their valuation of Chambejo Farms from $8.4 million to $4.8 million between December 2013 and August 2014? Is it the Assets Valuation Standards Committee of the Australian Property Institute? We will write to them and put the question.

The National Australia Bank commenced proceedings against the Cronin family and Chambejo Farms Pty Ltd to recover a debt and they failed. The extent of their failure was that it took their appointed receivers and managers, Ferrier Hodgson, the best part of three years to lose $4.5 million for for the National Australia Bank. So who explains that loss on the NAB balance sheet? Who, what person, what decision maker is called to account for and explain the loss and to whom do they have to explain themselves? Maybe in the world of the NAB it doesn’t matter how much customer blood is on the streets so long as the corporate profit of $6 billion is protected. Blood, as we have seen, is easily washed away.

What now? We have only just started. There are so many questions which as far as we can determine according to the law, Ferrier Hodgson and the National Australia Bank should answer. The campaign motto is ‘Persistence’.

Nothing in this world can take the place of persistence. Talent will not: nothing is more common than unsuccessful men with talent. Genius will not; unrewarded genius is almost a proverb. Education will not: the world is full of educated derelicts. Persistence and determination alone are omnipotent.

Calvin Coolidge.1872 – 1933.

I have been made aware that there are those who wish to comment, but for obvious reasons do not want their name publishing. I approve all comments before publishing and I will remove the writers name if they so wish. Anonymity is assured.

This is a comment from Facebook.

Clare-Bill Schoondergang

January 18 at 4:20pm

They most certainly do need to answer these questions ‘it’s appalling

Staggering story but unfortunately believable with the Banks involved. There are many similar stories from the Commonwealth takeover of Bankwest a few years back.

If it hasn’t been done already, this case needs to be presented to a very experienced investigative journalist, 4 Corners or perhaps 60 minutes or even the Australian Newspaper. Has the Financial Ombudsman Service had a look at the case? My non legal brain suggests that persistence will be rewarded here in terms of shaming the Bank and perhaps FH but that it won’t compensate the Cronins for destroying their lives. It’s here that justice is difficult to obtain because deep pockets win every time!!

name and address supplied. anonymity assured.

T h e H o n . B a r n a b y J o y c e M P

Minister for Agriculture and Water Resources Federal Member for New England

Ref: MC16-000299

Mr Roger Crook Global Farmer

Via email: roger.rankin.crook@bigpond.com

Dear Mr Crook

Thank you for your correspondence of 6 January 2016 regarding the National Australia Bank and its dealings with the Cronin family.

Recognising your concerns about this issue, you may be interested to learn that I have been working closely with the banking sector to ensure it supports customers for the long-term future of our farming communities. The Australian Government will continue to encourage banks to be fair, decent and patient with drought-affected farmers.

The Parliamentary Joint Committee on Corporations and Financial Services is undertaking an inquiry into the impairment of customer loans in relation to the practices of banks and other financial institutions. Should you be interested in following this inquiry, this can be done on the inquiry ‘s website at

http://www.aph.gov.au/Parliamentary _Business/Committees/Joint/Corporations_and_Financial_ Ser vices/customer_loans. The Committee’s report is due to be finalised by 31 March 2016 and

I look forward to its outcome.

Thank you again for your correspondence and for your concern and support for the Cronins. Yours sincerely

Barnaby Joyce MP

20 JAN 2016

In my view it is unprofessional, unethical and bad business to put the Cronin’s in such a position. Banks must realise that by providing such loans they are, in effect, becoming a partner investor and, as such, have a responsibility to to open, not secretive, and supportive. I see none of this in what I have read. Farming, by Australians, and for Australians, is critical for our country. Unless our politicians do something about this I fear that our farming sector will simply vanish.

Terry, wise words. All I ask is that you spread the word on this terrible situation and ask as many as possible to support us.

Thanks.

Roger